The average American has just $8,000 saved. That sounds manageable until you realize the average household spends $6,081 every single month.

Do the math. That’s barely two months of financial runway before things get genuinely difficult.

Here’s the part that stings even more—it’s not because people are reckless. According to the Federal Reserve’s 2024 Report on the Economic Well-Being of US Households, 21% of Americans have zero emergency savings. Thirty-seven percent cannot cover a sudden $400 expense without borrowing or selling something. These are not statistics about someone else. They’re about your street, your office, and quite possibly your own bank balance.

But there’s another side to that same data, one that rarely makes headlines. In 2024, for the first time in Bankrate’s annual savings poll, more Americans reported increasing their savings than decreasing them. Millennials saved an average of $9,299 in one year. Gen Z saved over $6,000. People with no extraordinary income, no inheritance, no financial windfall—just different decisions.

This guide is about those decisions. Twenty-one of them, built on real data, told through real stories, and ordered by how fast they actually produce results. Whether you’re starting from zero or trying to accelerate what you already have, this is how to save money in a way that sticks.

Table of Contents

Why Most People Struggle to Save Money—And It’s Not What You Think

Most advice on how to save money skips the honest part. The problem is rarely knowledge. Almost everyone knows they should spend less and save more. The problem is that saving feels like punishment when it has no clear purpose tied to it.

Research from the University of Scranton shows that people who set specific, written financial goals are significantly more likely to achieve them than those who hold vague intentions. The goal of “being responsible with money” doesn’t work. The goal of “having $4,000 in a separate account by March so I can visit Japan” does.

Before a single tip in this article will stick, answer one question: what specific thing are you saving for?

It doesn’t have to be grand. It can be three months of expenses sitting safely somewhere so you can sleep better at night. It can be a down payment. It can be the freedom to leave a job you hate without spiraling into debt. Name it. Write it somewhere. That single act changes how every strategy below feels—from restriction to progress.

For a complete framework on managing your money intentionally, see our complete guide to personal budgeting.

Where Your Money Is Actually Going Right Now

Before you can learn how to save money fast, you have to see where it’s leaving. Most people believe their money disappears on rent, food, and the occasional splurge. The real picture is more specific—and more fixable.

Bureau of Labor Statistics data shows the average American household spends approximately $1,200 per year on subscriptions they barely use, $3,900 per year eating lunch out on workdays, and over $4,000 on food delivery. A daily $6 coffee on weekdays adds $1,560 annually. None of these feel significant in the moment. Together they represent over $10,000 per year in almost entirely habitual spending—money that leaves on autopilot, not by deliberate choice.

That distinction matters. Habitual spending is the easiest kind to change because you only have to make the decision once.

Annual Cost of Common Habits

| Spending Habit | Annual Cost | Saving If Cut in Half |

|---|---|---|

| Daily coffee on weekdays ($6/day) | $1,560 | $780 |

| Lunch out on workdays ($15/day) | $3,900 | $1,950 |

| Food delivery twice a week | $4,000+ | $2,000 |

| Forgotten subscriptions | $1,560 | $780 |

| Total | $11,020+ | $5,510 |

Real People Who Learned How to Save Money Fast—And What Happened

Theory is easy. Here are three real people who figured out how to save money on a tight budget and changed their financial picture within twelve months. No extraordinary income. No luck. Just specific actions.

Sarah, 29—Nurse, Chicago

Starting position: $340 in savings | Income: $58,000

What changed: Canceled 9 forgotten subscriptions ($87/month), automated a $200 transfer on payday before touching her account, moved savings to a 4.5% APY high-yield account.

One year later: $3,180 saved. The first time in her adult life she had held more than $1,000 in any account.

“I kept waiting for the month where I had money left over. Once I automated it, I stopped waiting—the money was already there.”

Marcus, 34—IT Analyst, Atlanta

Starting position: $0 | Living paycheck to paycheck | Income: $74,000

What changed: Ran a 20-minute subscription audit, started meal planning (grocery bill fell from $680 to $420 per month), negotiated his internet bill down $45/month, began contributing enough to capture his full 401(k) employer match.

One year later: $7,800 in personal savings plus $4,200 in employer-matched retirement contributions he had been leaving unclaimed for three years.

“The employer match was the thing that made me angry at myself. I had been handing back $4,000 a year in compensation I was entitled to.”

Priya, 26—Freelance Designer, London

Starting position: £800 | Income: £42,000

What changed: Adopted a 50/30/20 budget, cooked at home five days a week instead of two, opened a high-interest ISA, introduced one no-spend day per week.

One year later: £6,400 saved. Credit card cleared. Investment account opened.

“One no-spend day a week sounds like a sacrifice. It turned out to be mostly about not buying things I would not have remembered buying.”

These are not exceptional people. The only thing that separates their results from the average is that they stopped trying to save what was left over and started designing a system that saved first.

To build your own saving system, start with our guide on how to create a monthly budget from scratch.

Where You Stand Right Now—Savings Benchmarks and Growth Projections

Understanding how to save money effectively means first knowing where you are relative to where you should be.

Savings Benchmark by Age Group

Based on the Federal Reserve Survey of Consumer Finances 2024 and Vanguard How America Saves 2025:

| Age Group | Median Savings (US) | Recommended Target | Gap Reality |

|---|---|---|---|

| Under 25 | $2,000–$4,000 | 3 months’ expenses (~$18,000) | Very High |

| 25–34 | $5,400 | 1x annual salary | High |

| 35–44 | $41,540 | 3x annual salary | Medium |

| 45–54 | $71,130 | 6x annual salary | Medium |

| 55–64 | $185,000+ | 8–10x annual salary | Low–Medium |

| 65+ | $272,000+ | Full retirement fund | Depends |

Most people fall short of these benchmarks—not because they’re bad with money, but because nobody ever showed them a clear system for how to save money consistently over time.

What Different Savings Rates Produce Over Time

Based on a monthly take-home pay of $3,500. Figures exclude investment growth or interest earnings.

| Year | Save 5% ($175/mo) | Save 10% ($350/mo) | Save 15% ($525/mo) | Save 20% ($700/mo) |

|---|---|---|---|---|

| Year 1 | $2,100 | $4,200 | $6,300 | $8,400 |

| Year 3 | $6,300 | $12,600 | $18,900 | $25,200 |

| Year 5 | $10,500 | $21,000 | $31,500 | $42,000 |

| Year 10 | $21,000 | $42,000 | $63,000 | $84,000 |

Add 4–5% annual interest from a high-yield savings account and the 10-year figures grow by an additional $5,000–$18,000 on top of these numbers.

The difference between saving 10% and 20% over ten years is $42,000 on the same income. The difference between saving nothing and saving 5% is $21,000. Neither requires a raise. Both require a system.

For the complete framework on building that system, see our personal budgeting guide.

The 21 Strategies—How to Save Money Fast, in Order of Results

Strategy 1—Pay Yourself First, Before You Can Spend It

Every serious financial planner, every study on long-term savings behavior, and every person who has actually managed to save consistently arrives at the same conclusion: automate savings the moment your paycheck arrives. Not what’s left over. The first transfer out.

Set up an automatic transfer from your checking account to a separate savings account for the exact day your salary deposits. NerdWallet’s 2025 savings survey found that 25% of consistent savers have money deposited directly from payroll, bypassing their checking account entirely. That group saves more than any other category surveyed.

The reason this works is simple. Your brain adjusts to living on whatever remains after the transfer, the same way it adjusted to taxes coming out before you ever saw the money.

This is the core principle behind the “Pay Yourself First” budgeting method. For more on this and other budgeting approaches, read our complete personal budgeting guide.

Action step: Log into your bank today. Set up a recurring automatic transfer for your next payday. Start with whatever feels slightly uncomfortable but realistic.

Strategy 2—The Subscription Audit That Pays You Immediately

C+R Research found the average household underestimates its monthly subscription spending by over $130. That’s more than $1,500 per year in recurring charges people are paying without consciously choosing to.

Open the last two months of your bank and credit card statements. Highlight every recurring charge—monthly, annual, and anything that looks unfamiliar. For each item, ask one question: Did I actively use this in the past 30 days? Not “could I use it”—did I.

Cancel everything that fails that test. You can resubscribe to anything later. Sarah canceled nine subscriptions in one sitting and hasn’t missed a single one. Her monthly saving: $87. Her annual saving: $1,044 for twenty minutes of work.

For tools that help track and manage subscriptions automatically, see our guide to the best budgeting apps.

Action step: Schedule 20 minutes this week to review one month of statements. Cancel at least three recurring charges you didn’t use last month.

Strategy 3—Stop Letting Your Savings Earn Almost Nothing

The average traditional savings account in the US currently pays 0.40% APY (FDIC data). High-yield savings accounts at online banks are offering between 4.0% and 5.0% APY right now.

On $5,000 saved, the difference is $20 per year versus $225 per year. On $20,000, it’s $80 versus $900+. Same money. Same risk. Zero additional effort. Just a different account.

A Motley Fool survey found 22% of Americans didn’t know accounts yielding over 4% existed. You can keep your current bank for day-to-day spending and keep your savings somewhere that actually earns. These are not competing decisions.

Action step: Search for the best high-yield savings account available in your country. Open one this week. Transfer your savings there. The process takes fifteen minutes and the benefit is permanent.

Strategy 4—Meal Planning Cuts Food Costs by 20–30% Without Eating Worse

US food costs rose over 22% between 2021 and 2025. Despite that, most households still walk into a supermarket with no plan, buying by instinct, and discovering mid-week that half of it has gone to waste. The USDA estimates food waste costs the average American household $1,500 per year.

Research from Cornell’s Food and Brand Lab found that people who plan meals in advance spend 20–30% less on groceries with no reduction in food quality or satisfaction. Marcus dropped his monthly grocery bill from $680 to $420—a $3,120 annual saving—simply by writing seven meals on a notepad before shopping and buying only what those meals required.

The method doesn’t need to be complex. Seven meals, one shopping list, nothing off-script. That’s the whole system.

For more strategies on reducing food costs, read our guide on how to save money on a tight budget.

Action step: Before your next grocery run, write seven dinners. Build a list from those meals. Buy only what’s on that list.

Strategy 5—The 30-Day Rule Quietly Kills Impulse Buying

Impulse spending accounts for an estimated 40–80% of all purchases depending on the product category. Every e-commerce platform on earth is engineered specifically to collapse the distance between impulse and purchase—countdown timers, “only 2 left”, one-tap checkout.

The counter is almost insultingly simple. When you feel the urge to buy something non-essential, add it to a dedicated list with today’s date. Wait 30 days. Then decide.

The research behind this is consistent. Most impulse urges dissolve within 48–72 hours once any friction is introduced. Priya tried this for one month and added 23 items to her list. She bought two of them. The other 21 she had already forgotten.

To understand the psychology behind impulsive purchases, read our guide on how to stop overspending.

Action step: Open a note on your phone right now and label it “Want List.” Next time you feel the urge to buy something non-essential, add it there. Review the list in 30 days.

Strategy 6—Negotiate Your Bills—Most Providers Will Say Yes

Internet providers, phone carriers, and insurance companies all maintain retention budgets—money specifically allocated to prevent customers from canceling. When you call and ask for a better rate, you’re drawing from a fund designed for exactly that purpose.

A 2024 Consumer Reports survey found that 70% of people who called to negotiate a bill received a discount or a better offer. The average saving per successful negotiation: $20–$50 per bill per month.

Three bills negotiated, one hour of calls, $90/month saved—that’s $1,080 every year for conversations you could have this week. The script is one sentence: “I’ve been a loyal customer for [X years] and I’ve seen lower rates with other providers. Is there anything you can do on my current rate?”

Action step: Identify your three highest monthly service bills. Call each provider this week and ask that one question.

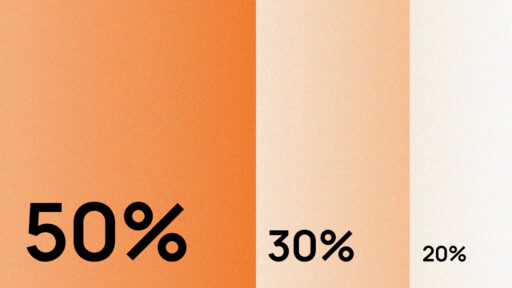

Strategy 7—The 50/30/20 Budget—Three Numbers, Not Forty

Most budgets collapse because they require tracking dozens of spending categories in perpetuity. The 50/30/20 rule works because it requires exactly three.

- 50% of take-home pay covers needs—rent, utilities, groceries, transport, insurance, and minimum debt payments

- 30% covers wants—dining out, entertainment, travel, subscriptions you actively use

- 20% goes directly to savings and extra debt repayment

The Bureau of Labor Statistics data shows the average American currently saves 4.4% of disposable income. The 50/30/20 framework targets 20%. On a $50,000 income, the gap between those two numbers is $400–$900 per month in additional savings—money that exists in the budget but is not currently being directed anywhere productive.

For a complete breakdown of whether this method works for your situation, read our full guide: The 50/30/20 Rule—Does It Actually Work?

Action step: Calculate last month’s total take-home pay. Sort your spending into the three buckets. Identify which bucket is over its allocation and by how much.

Strategy 8—Build an Emergency Fund Before Anything Else

This is the most important strategy in this article and the least exciting one, which is exactly why it belongs here rather than at the top where nobody would believe it.

Without an emergency fund, every unexpected expense becomes a debt spiral. A $900 car repair goes on a credit card at 24% APR. It takes months to pay off. By the time it’s cleared, that $900 expense has cost over $1,050. Two emergencies in one year and you’ve added $2,400 in interest to bills that were already stressful enough without it.

The Federal Reserve’s 2024 survey found that 55% of US adults had set aside at least three months of emergency savings. That means 45% had not. Financial security experts broadly recommend covering three to six months of essential expenses. If that number feels overwhelming, aim for $500 first. Then $1,000. Then one full month of expenses. Each milestone materially reduces your vulnerability and the chronic low-grade financial anxiety that comes with it.

For the complete framework on emergency fund targets and where to keep them, read: Emergency Fund—How Much You Really Need

Action step: Calculate one month of your essential expenses. Open a separate savings account, name it “Emergency Fund,” and set up a monthly transfer toward that first target.

Strategy 9—Capture Every Dollar of Your Employer’s Match

If your employer offers a 401(k) match or pension contribution match and you’re not contributing enough to capture the full amount, you’re leaving your own compensation uncollected. This is not a metaphor. The money is budgeted for you. You are declining to take it.

Vanguard’s How America Saves 2025 report puts the average employer contribution match at 4.4% of salary. On a $60,000 income, an uncaptured match is $2,640 per year. Over 20 years with standard market growth, leaving it uncaptured can cost over $100,000 in retirement wealth.

Marcus had done this for three years when he realized it. It remains, in his own words, the financial decision he regrets most.

Action step: Check your benefits portal or call HR today. Find your employer’s exact match rate. Increase your contributions to at least capture it fully.

Strategy 10—Cook at Home More Than You Order

The numbers here are hard to ignore. Food delivery twice a week averages $35–$55 per order once fees, service charges, and a tip are included—that’s $3,640–$5,720 per year. Coffee out every weekday: $1,560. Lunch on workdays: $3,900.

The average home-cooked meal costs $4–$8 per person (USDA). The average US restaurant meal in 2024 cost $23.50 per person (National Restaurant Association). That’s a three-to-one difference for the same meal.

Priya reduced delivery from five nights per week to one. Monthly saving: $340. Annual: $4,080. She still eats well. She still orders on Friday. She simply stopped letting it be the path of least resistance at 7pm on a Tuesday.

For additional strategies on reducing food costs without sacrificing quality, see our guide on saving money on a tight budget.

Action step: Choose three nights per week to cook at home instead of ordering. Batch cook on Sunday so weeknight cooking requires less time and effort.

Strategy 11—Cashback Cards Work, But Only With Iron Discipline

Cashback credit cards return 1–3% on every purchase. On $2,000 in monthly spending, that’s $240–$720 per year in money that comes back to you simply for using a card you would have used anyway.

The one condition: pay the full balance every single month without exception. The moment you carry a balance at 20–28% APR, every dollar of cashback earned is erased and then some. If you currently carry a balance, pay it off before pursuing this strategy. Once you’re paying in full every month, not using a cashback card is leaving free money uncollected.

Action step: Check whether your current credit card earns cashback or rewards. If not, research cards offering cashback on grocery and fuel purchases—the categories that generate the most consistent returns.

Strategy 12—Sell What You’re Not Using This Month

The average American household contains $300–$3,000 in unused, sellable items—electronics, unworn clothing, unused fitness equipment, books, kitchen appliances in the back of a cupboard. This is not a long-term money-saving strategy. It’s a one-time momentum builder.

Sarah sold a stationary bike, two unopened tech gift items, and 40 pieces of clothing across two weekends. Total: $870. That became her starter emergency fund—the financial buffer that changed her relationship with money from that point forward.

Action step: Walk through your home and identify ten items you haven’t used in the past year. List three of them online this week—Facebook Marketplace, eBay, Poshmark, or Craigslist.

Strategy 13—The Energy Audit That Costs Nothing to Run

Energy bills feel like fixed costs. They’re not.

Switching to LED bulbs reduces lighting electricity use by up to 75% per bulb. Adjusting your thermostat by 2°F in either direction reduces heating and cooling costs by approximately 6% per degree, according to the US Department of Energy. Unplugging devices on standby—televisions, gaming consoles, phone chargers, kitchen appliances—eliminates the phantom load that accounts for 5–10% of household electricity use.

Total saving from all three adjustments: $360–$600 per year. One-time decisions. Zero ongoing maintenance. No change to how you live.

Action step: Replace the five most-used bulbs in your home with LED equivalents. Plug entertainment electronics into a switchable power strip. Turn it off when not in use.

Strategy 14—One No-Spend Day Per Week Rewires More Than Your Spending

A no-spend day—one day per week with zero purchases—is not about the amount saved on that specific day. It’s about what happens to your awareness the other six days.

Most spending is automatic. You walk past a coffee shop and your hand is already reaching for your phone before you’ve consciously thought about it. A no-spend day interrupts that pattern and creates a moment of deliberate decision where there usually is none. Over time, that deliberateness starts bleeding into the rest of the week.

Financial behavior research consistently finds that people who observe regular no-spend days save an additional $150–$300 per month without making any other changes to their budget.

To build this into a structured financial system, consider implementing zero-based budgeting, which assigns every dollar a purpose.

Action step: Choose one day this week as a no-spend day. After four consecutive weeks, calculate the total amount you would otherwise have spent. That number will tell you whether to continue.

Strategy 15—Negotiate Your Rent at Renewal

Most people accept rent increases at lease renewal without question. Almost nobody thinks of it as negotiable. It is.

Landlord turnover costs—cleaning, repairs, lost rent during vacancy, advertising—typically run $1,000–$3,000 per unit. A reliable, on-time-paying tenant asking for no increase or a modest reduction is substantially cheaper than finding a replacement. You have more leverage than you think.

At your next renewal, note your track record as a reliable tenant, reference comparable rents in the area, and ask respectfully for either a reduction or no increase. A $50/month reduction is $600 per year. A $100/month reduction is $1,200.

Action step: At your next lease renewal, look up comparable rents on Zillow or a local property site. If the case exists, make it in writing.

Strategy 16—Switch to Generic Brands on Staple Items

The FDA requires generic medications to contain the same active ingredients as name-brand equivalents. For most grocery staples, cleaning products, and basic personal care items, store-brand products meet identical specifications—frequently manufactured in the same facilities as the branded versions.

The price difference is consistently 20–40% lower. Consumer Reports data shows switching to store brands across regular grocery purchases saves a family of four $80–$150 per month. Annually: $960–$1,800 per year for zero quality reduction on most items.

The categories where generics perform identically: OTC medications, canned goods, baking ingredients, cleaning products, most frozen foods, basic personal care. Keep your preferred brands where quality genuinely matters to you. Switch everything else.

Action step: On your next grocery run, choose the store-brand version of five items you normally buy branded. Compare the result. You’ll likely not notice a difference.

Strategy 17—Compare Prices Automatically on Every Online Purchase

For any purchase over $100, five minutes of price comparison across retailers almost always finds a lower option. Browser extensions like Honey or Capital One Shopping do this automatically—scanning multiple retailers and applying available coupons at checkout without any action required from you.

Honey’s own data suggests users save an average of $28 per order when a saving is found. Across 20 purchases per year, that’s $560 returned to you automatically with zero ongoing effort.

Action step: Install a free price comparison browser extension today. It requires no maintenance and activates silently on every online purchase.

Strategy 18—Travel for Less Without Traveling Less

The same flight on the same route on the same day can cost 40–60% less depending on when you book and which day you fly. This is not a myth—it’s how airline revenue management systems are designed.

What consistently works: Book domestic flights 4–8 weeks out, international flights 3–5 months out. Fly Tuesday or Wednesday rather than Friday or Sunday. Use Google Flights’ calendar view to find the cheapest date within a flexible range. Set fare alerts for trips you’re planning months ahead through Google Flights or Hopper.

A family of four booking two weeks earlier than last-minute typically saves $200–$600 on a single round trip.

Action step: For your next planned trip, spend ten minutes on Google Flights’ calendar view. Check whether shifting your dates by one or two days produces a meaningful price difference.

Strategy 19—Understand the Real Annual Cost of Daily Habits

The concept of small daily purchases compounding into large annual figures gets dismissed as oversimplified. The dismissal is wrong.

| Daily Habit | Annual Cost at Current Rate |

|---|---|

| $6 coffee on weekdays (260 days) | $1,560 |

| $15 lunch out on workdays (260 days) | $3,900 |

| $30 weekly unplanned online order | $1,560 |

| Total | $7,020 |

The goal is not to eliminate these. It’s to choose them deliberately rather than by default. Your morning coffee may be one of the genuine small pleasures in your day—keep it. But make that choice on purpose, and ask which other automatic habits are worth keeping at that cost.

Cutting any single category by half saves $780–$1,950 per year with minimal change to daily life.

For a complete framework on understanding where money goes and how to redirect it, see our personal budgeting guide.

Action step: Identify your one highest-frequency, lowest-satisfaction spending habit. Reduce it by 50% for 30 days and calculate the annual saving.

Strategy 20—Check Your Credit Report for Errors This Week

A 2021 Federal Trade Commission study found approximately one in five Americans has at least one error on their credit report. These errors—accounts that aren’t yours, wrongly reported late payments, incorrect balances—can suppress your credit score by 50–100 points without your knowledge.

A lower credit score means higher interest rates on every loan you ever take. The difference between a good and excellent credit score on a $300,000 mortgage can amount to $40,000–$80,000 in extra interest paid over the loan’s lifetime. That’s not a small number. And many people are paying it unnecessarily.

You can access all three credit reports for free at AnnualCreditReport.com—the only site officially authorized under US federal law. Review reports from Equifax, Experian, and TransUnion. Dispute any inaccuracy directly with the relevant bureau.

Action step: Visit AnnualCreditReport.com this week. Download all three reports. Spend 20 minutes reviewing them for anything that looks incorrect.

Strategy 21—Add a Second Income Stream—Because Cutting Has a Ceiling

There’s a mathematical floor on savings from expense reduction. You cannot spend below zero. But income has no ceiling.

Even $200–$500 per month in additional income transforms what’s achievable in a savings plan. At $500 extra per month, you add $6,000 per year to your savings without changing a single existing expense.

The Bureau of Labor Statistics reported in 2024 that approximately 36% of Americans have some form of supplemental income outside their primary job. The median in that group: $6,000–$8,000 per year. The most accessible routes: freelancing in your professional field, tutoring any subject, selling unused items, food or grocery delivery on weekends, renting a parking space or spare room.

None of these are glamorous. All of them work.

Action step: Identify one skill or asset you have that could generate $100–$200 per month outside your main job. Take one concrete step toward it this week—not next week. This week.

If You Only Do Three Things This Week

You don’t need to action all 21 strategies at once. Here are the three with the highest immediate, lasting impact—each taking under 30 minutes.

First—Open a high-yield savings account today. Move your existing savings there. You’ll immediately begin earning 10–20x more interest with zero ongoing effort. Fifteen minutes now, permanent benefit from this month forward.

Second—Set up an automatic transfer for your next payday. Even $50. The habit of saving money consistently matters more than the amount when you’re starting. You’ll naturally adjust to spending what remains.

Third—Review one month of statements and cancel unused subscriptions. Most people find $40–$150 in forgotten recurring charges during this single 20-minute exercise. That’s $480–$1,800 returned to your budget annually for one sitting.

Three actions. Roughly 45 minutes total. Your financial position will be measurably different by the end of this month.

For the complete system that connects all these strategies together, read our step-by-step guide to creating a monthly budget.

The Honest Closing

Learning how to save money is not about becoming a different kind of person. It’s not about sacrifice or giving up things that make life enjoyable.

It’s about building systems that work for you in the background. Automated transfers that save before you can spend. Accounts that earn real interest instead of almost nothing. Subscriptions canceled once rather than paid forever. Decisions made once that pay you every single month without requiring ongoing willpower.

Americans who save consistently report saving 15–23% of their take-home income. Not because they earn more. Because their systems do the work.

You can build those systems. The best time to start was a year ago. The second best time is today.

Ready to build your complete financial system? Start with our comprehensive guide to personal budgeting to create the framework that makes consistent saving possible.

Frequently Asked Questions

What is the fastest way to save money when you’re broke?

The fastest approach when money is very tight is to focus on actions you take once that produce ongoing savings automatically. Cancel unused subscriptions (average saving: $40–$130/month), call your biggest service providers and ask for a lower rate (average saving per successful call: $20–$50/month), and move any savings you have to a high-yield savings account earning 4–5% APY instead of 0.40%. These three steps require no ongoing willpower and deliver immediate, recurring monthly results.

For additional strategies that work on extremely tight budgets, see our complete guide on how to save money on a tight budget.

How much of my paycheck should I save each month?

Financial advisors widely recommend 20% of take-home pay, as suggested by the 50/30/20 rule. NerdWallet’s 2025 survey found the working American median is closer to 15%. If 20% feels unreachable right now, start with whatever percentage you can sustain—even 5% of a $3,000 monthly take-home is $1,800 per year. The habit of saving money regularly matters more than the specific percentage when you’re getting started. Increase by 1–2% every six months as your income grows or your fixed expenses decrease.

What expenses should I cut first to save money fast?

Start with forgotten subscriptions—they’re the most painless cuts available and most households save $40–$130 per month from a single audit. Second, look at food delivery and eating out, which tends to be both high-spending and highly reducible with minimal impact on quality of life. Avoid cutting things that genuinely support your health, productivity, or wellbeing. Unsustainable cuts lead to rebound spending that leaves you worse off than before.

For a complete framework on identifying which expenses to cut and in what order, read our personal budgeting guide.

How can I save money with no savings experience at all?

Remove willpower from the equation completely. Open a separate savings account—ideally a high-yield one—and set up an automatic transfer for the same day your paycheck arrives. Even $25 per transfer. Your spending will adjust to whatever remains, the same way it adjusted to any other fixed monthly cost. Add one money-saving strategy per week from that point. Stack small wins instead of attempting a complete overhaul—the evidence strongly favors incremental progress over ambitious restarts.

To build a complete beginner-friendly system, start with our guide on how to create a monthly budget from scratch.

Do small daily purchases really add up to that much?

Yes. A $6 daily coffee on weekdays costs $1,560 per year. Lunch out on workdays averages $3,900 per year. One weekly unplanned delivery order at $30 adds $1,560 per year. Together that’s $7,020 annually in largely unconsidered spending. The goal is not to eliminate these habits—it’s to choose them deliberately rather than by default. Reducing any single category by half saves $780–$1,950 per year with minimal lifestyle change.

To understand how these small purchases fit into your overall spending pattern, see our guide on understanding why you overspend.

How do I track my savings progress?

The simplest method is a dedicated high-yield savings account with a clear name (“Emergency Fund,” “House Deposit,” etc.) where you can watch the balance grow. Many people find success using budgeting apps that connect to your accounts and track savings automatically, or using free budget spreadsheet templates for manual tracking. The key is choosing a system you’ll actually check regularly—weekly is ideal.

Should I pay off debt or save money first?

Build a small emergency buffer first—$500 to $1,000—to prevent new debt from unexpected expenses. Then focus on high-interest debt (credit cards above 15% APY) while maintaining minimum payments on everything else. Once high-interest debt is cleared, split your attention between building a full emergency fund and paying down remaining debt. For couples navigating this decision together, see our guide on how to budget as a couple.

Sources

All statistics and data in this guide are sourced from the following verified sources:

- Federal Reserve Report on the Economic Well-Being of US Households 2024

- Vanguard How America Saves 2025

- Bankrate Annual Savings Survey 2025

- NerdWallet Savings Report 2025

- Bureau of Labor Statistics Consumer Expenditure Survey

- FDIC National Rates Data

- USDA Food Loss and Waste

- FTC Credit Report Study 2021

- Consumer Reports Bill Negotiation Survey 2024

- C+R Research Subscription Economy Study

- National Restaurant Association 2024

- Cornell Food and Brand Lab

- University of Scranton Goal-Setting Research

- Motley Fool Consumer Finance Survey

Ready to put these strategies into action? Start by creating your complete personal budget to ensure every dollar you save has a clear purpose.