Most people think they already know roughly where their money goes. They are almost always wrong.

Studies consistently find that people underestimate their monthly spending by $200 to $400—not because they are dishonest, but because small, frequent purchases are psychologically invisible. The $14 lunch that doesn’t feel like lunch because you ate at your desk. The $8 app subscription you forget exists until the statement arrives. The delivery fee that appeared on four different Tuesdays.

86% of Americans say they budget. Yet 69% are now living paycheck to paycheck—a new high in seven years of tracking this data.

That gap tells you something important: the problem for most people is not the absence of a budget. It’s the absence of a budget built on what is actually happening with their money, rather than what they wish was happening.

This guide shows you exactly how to build a monthly budget from scratch—step by step, with real numbers, real templates, and every common mistake named and explained so you can skip past the parts where most people quit.

If you’ve never learned how to build a monthly budget properly, this is your starting point. By the end of this page, you will have a working first budget—not a theory of one.

Table of Contents

What Is a Monthly Budget?

A monthly budget is a forward-looking financial plan that allocates your after-tax income across fixed expenses, variable spending, savings, and debt repayment before the month begins. It tells your money where to go before it leaves your account—not a record of where it went last month.

Why Building a Monthly Budget From Scratch Actually Works

Before the steps, understand what a monthly budget genuinely does—and does not do.

Learning how to make a monthly budget can be a key step toward solidifying your financial status and future. According to the Federal Reserve’s Survey of Consumer Finances, nearly 40% of Americans cannot cover a $400 emergency expense without borrowing. A monthly budget is a simple and effective way of managing or avoiding debt—the reason millions of Americans find themselves weighed down with hefty interest payments is that they spend more each month than they bring in.

The practical benefits are well-documented:

A budget plays a valuable role in determining how much of your income you need to save each month to reach your goals—whether that is a down payment on a car next year, a home in five years, or building up your retirement nest egg.

A budget can also help anticipate expenses like car costs, utilities, or phone bills—and prepare you for a rainy day.

None of this requires a finance degree, spreadsheet expertise, or an extraordinary income. It requires two honest numbers—what comes in and what goes out—and a system for aligning them.

For the complete framework that connects all budgeting methods together, see our complete guide to personal budgeting.

Monthly Budget in 7 Steps (Quick Overview)

Here’s how to build a monthly budget from scratch:

- Calculate real take-home income — Use net pay, not gross salary

- List fixed expenses — Every recurring obligation

- Average variable expenses — Three months of statements, not estimates

- Add savings first — Before discretionary spending

- Assign spending categories — Allocate remaining funds

- Choose tracking system — App, spreadsheet, or paper

- Review and adjust monthly — Make one improvement each month

What You Need Before You Start—The Honest Preparation

Most budgeting guides tell you to “gather your financial information.” Here is exactly what that means in practice, and why each piece matters.

1. Three Months of Bank and Credit Card Statements

Not one month. Three. A single month captures whatever happened to be unusual that month—a birthday, a car expense, a one-off purchase—and makes it look like normal spending. Three months averages out the noise and shows you what your actual spending patterns look like.

For any category where your outlay is not fixed, determine the average by looking back over the past three months of spending. If you spend an average of $433 on groceries each month, you can round up to $450.

Download your last three months of statements from every account you use. Every credit card, every debit account, every payment platform. A purchase on PayPal is still spending. A subscription charged to a card you rarely check is still spending.

2. Your Real Take-Home Pay—Not Your Salary

The first step is knowing your net income—the actual amount of money you bring home after taxes, insurance, and other deductions. Only work with take-home pay. Never budget using your gross salary.

A $55,000 annual salary is approximately $3,800–$4,200 monthly take-home after federal tax, state tax, and Social Security deductions—not $4,583. Budgeting from gross overstates your available income by 15–25% before you have written a single category.

If you are a salaried employee, your net take-home pay should be listed on your payslip. Since state and federal income tax and Social Security are withheld, it will be significantly smaller than your gross income. If you are enrolled in a health insurance plan, FSA, or 401(k), funds for those accounts will usually be withdrawn automatically as well.

3. A List of Every Regular Obligation

Before categorizing anything, write down every fixed commitment—rent, car payment, insurance premiums, subscriptions, phone contract, minimum debt payments. These are non-negotiable. They form the immovable base of your budget before any variable spending is considered.

Step 1—Calculate Your Real Monthly Income

Start with your monthly after-tax income as your spending limit for each month.

Fill in every source of income that reliably arrives each month:

| Income Source | Monthly Amount (After Tax) |

|---|---|

| Primary job—net take-home | $ |

| Partner’s income (if budgeting jointly) | $ |

| Side income or freelance (use 3-month average) | $ |

| Rental income | $ |

| Benefits or regular transfers | $ |

| Any other consistent monthly income | $ |

| Total Monthly Income | $ |

If Your Income Varies Month to Month

If your income varies from month to month, use an average based on the last year—or start with your low-earning month of that year as a baseline.

Budgeting from a conservative floor protects you in slow months. Any income above your baseline in higher-earning months becomes surplus—which goes directly to savings first, wants second.

Step 2—List Every Monthly Expense

The biggest lift in budgeting is getting an accurate accounting of your monthly expenses. This step is where most people underperform—not through dishonesty, but through optimism. The goal is accuracy, not aspiration.

Fixed Expenses First

Fixed expenses are the same or nearly the same every month. They don’t require decision-making. They are commitments you have already made.

| Fixed Expense | Monthly Amount |

|---|---|

| Rent or mortgage | $ |

| Car payment | $ |

| Car insurance | $ |

| Health insurance (your portion) | $ |

| Life or renters insurance | $ |

| Phone contract | $ |

| Internet plan | $ |

| Minimum credit card payments | $ |

| Student loan minimum payment | $ |

| Any other loan minimums | $ |

| Childcare or school fees | $ |

| Streaming and subscription services | $ |

| Gym or fitness membership | $ |

| Any other fixed monthly commitments | $ |

| Total Fixed Expenses | $ |

Important: Don’t leave subscriptions out because you’ve forgotten some. Go through your statements line by line. More than 86% of people have a budget, yet the average American household spent $77,280 in 2023—a 51% increase from 2013. Subscription creep is one of the most consistent contributors to that growth.

For strategies on identifying and eliminating forgotten subscriptions, see our guide on how to save money fast.

Variable Expenses Next

Variable expenses, such as how much you spend on gas or eating out, will fluctuate from month to month. Use your three-month statement average for each category—not your best guess.

| Variable Expense | 3-Month Average | Monthly Budget Target |

|---|---|---|

| Groceries | $ | $ |

| Fuel and transport costs | $ | $ |

| Dining out and food delivery | $ | $ |

| Entertainment and activities | $ | $ |

| Clothing and personal care | $ | $ |

| Medical and pharmacy costs | $ | $ |

| Household supplies | $ | $ |

| Gifts and celebrations | $ | $ |

| Children’s activities and supplies | $ | $ |

| Miscellaneous / cash spending | $ | $ |

| Total Variable Expenses | $ | $ |

The column that matters most: The gap between your three-month average and your budget target in the variable column. If you’ve been spending $480 on dining out but your budget targets $250, that gap is the work—and it’s where most monthly budget savings come from.

Step 3—Do the Core Calculation

Once you have your totals, the budget equation is simple:

Monthly Income − Fixed Expenses − Variable Expenses = Surplus or Deficit

| Your Number | Amount |

|---|---|

| Total Monthly Income | $ |

| Minus Total Fixed Expenses | − $ |

| Minus Total Variable Expenses | − $ |

| Monthly Surplus or Deficit | = $ |

If the result is positive: You have a surplus. The question is where it is currently going—because if you’re not directing it intentionally toward savings or debt repayment, it’s almost certainly disappearing into variable spending without you noticing. This is the most common scenario.

If the result is negative: You are spending more than you earn each month. This is a mathematical problem that has only two solutions: reduce expenses or increase income. There is no budgeting technique that makes a deficit disappear—the budget simply makes it visible so you can address it.

If your monthly expenses exceed your income, you will need to make adjustments—starting with variable expenses or reviewing unnecessary fixed costs like unused subscriptions.

Step 4—Add Your Savings Line Item—Before Anything Else

This is the step that separates budgets that build wealth from budgets that simply track spending.

Before you allocate anything to wants or discretionary spending, your monthly budget must include a savings line item—a specific dollar amount that moves automatically from your checking account to a savings or investment account on payday.

The reason this goes in before wants rather than after: The overwhelming majority of Americans say budgeting has helped them get out of—or stay out of—debt. The ones it helps most are those who treat savings as a fixed, non-negotiable obligation rather than the leftover from a month of spending.

| Savings Category | Monthly Target | Where It Goes |

|---|---|---|

| Emergency fund (until 3 months built) | $ | High-yield savings account |

| Retirement contributions (above employer match) | $ | 401(k) or IRA |

| Short-term goal (house deposit, car, travel) | $ | Separate named savings account |

| Extra debt repayment (above minimums) | $ | Highest-interest debt first |

| Total Monthly Savings | $ |

Not sure how much emergency fund to build or where to put your savings? Read: How to Build an Emergency Fund From Zero

Step 5—Assign the Remainder to Spending Categories

With income calculated, fixed expenses listed, savings allocated, and variable expenses averaged—now assign your remaining budget to spending categories for the month.

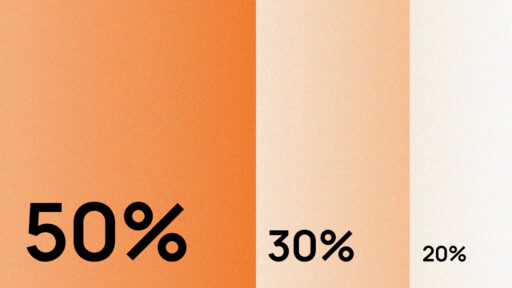

This is where your chosen budgeting method shapes the structure. If you’re using the 50/30/20 rule, your categories should fall within those three proportional buckets. If you’re using zero-based budgeting, every unassigned dollar needs a category until income minus all assignments equals zero.

Monthly Budget vs 50/30/20 Rule—What’s the Difference?

A monthly budget is a framework for allocating income across all expenses and savings categories. The 50/30/20 rule is a specific budgeting method that divides your budget into three proportional buckets: 50% needs, 30% wants, 20% savings.

When to use the 50/30/20 rule: If you want a simple, percentage-based structure with minimal category tracking. Best for beginners and people with moderate incomes in mid-cost-of-living areas.

When to use a detailed monthly budget: If your income is irregular, your housing costs exceed 50% of income, or you have specific aggressive savings or debt payoff goals that require more granular control.

Can you use both? Yes. Many people build a detailed monthly budget that follows the 50/30/20 percentage framework—using the percentages as guardrails while tracking specific categories within each bucket.

For a complete comparison of budgeting methods, see our complete guide to personal budgeting.

A Complete Sample Monthly Budget

Using these steps, here’s how a budget might work for someone with median US household monthly take-home pay. This example is based on a single-income household with $3,800 monthly take-home.

| Category | Budget | % of Income | Bucket |

|---|---|---|---|

| SAVINGS FIRST | |||

| Emergency fund contribution | $300 | 7.9% | Savings |

| Retirement (above employer match) | $200 | 5.3% | Savings |

| Short-term savings goal | $200 | 5.3% | Savings |

| FIXED NEEDS | |||

| Rent / mortgage | $1,150 | 30.3% | Needs |

| Car payment | $250 | 6.6% | Needs |

| Car insurance | $120 | 3.2% | Needs |

| Health insurance (employee share) | $90 | 2.4% | Needs |

| Phone plan | $45 | 1.2% | Needs |

| Internet | $55 | 1.4% | Needs |

| Minimum debt payment | $80 | 2.1% | Needs |

| VARIABLE NEEDS | |||

| Groceries | $380 | 10% | Needs |

| Fuel | $120 | 3.2% | Needs |

| WANTS | |||

| Dining out and delivery | $160 | 4.2% | Wants |

| Entertainment | $80 | 2.1% | Wants |

| Subscriptions (used) | $45 | 1.2% | Wants |

| Personal care and clothing | $70 | 1.8% | Wants |

| Miscellaneous buffer | $80 | 2.1% | Wants |

| Remaining (rolled to savings) | $375 | 9.9% | Savings |

| TOTAL | $3,800 | 100% |

What this budget produces:

- Monthly savings total: $1,075 ($700 intentional + $375 surplus)

- Annual savings at this rate: $12,900

- Emergency fund fully funded: within 5–6 months

Step 6—Choose Your Tracking Method

A budget built but not tracked is a plan that exists only on paper. The tracking step is where the budget meets real life—and where most first-time budgeters abandon the process.

The most important finding from budgeting behavior research: The frequency of checking your budget matters more than the sophistication of the tool you use. Weekly check-ins—even 10 minutes—consistently outperform monthly reviews in terms of staying on plan and catching overruns before they compound.

Research shows that 27% of young adults prefer budgeting apps, while 39% of middle-aged adults favor spreadsheets, and 43% of older adults stick to pen and paper. Every method works. The right tool is the one you will actually open.

| Tool | Best For | Biggest Advantage |

|---|---|---|

| Budgeting app (Monarch, YNAB, Rocket Money) | Automatic trackers | Bank syncing, real-time categorization |

| Google Sheets or Excel | Detail-oriented customizers | Free, fully flexible, no subscription |

| Printed budget worksheet | Visual, tactile learners | Tangible, no screen required |

| Pen and paper envelope | Cash-based spending | Immediate, physical limit awareness |

Want automatic tracking instead of spreadsheets? See our full breakdown of the best budgeting apps and which one fits your personality.

For free templates you can use immediately: Best Free Budget Spreadsheet Templates

Step 7—Review and Adjust at the End of Month One

Your first monthly budget will not be perfect. This is not a failure—it’s the expected and necessary first iteration.

Budgets are not rigid—they are living documents. If you overspend in one category, don’t panic. Make adjustments. The goal is not perfection, but progress.

At the end of month one, sit down with your budget and actual spending side by side. Record your spending daily or weekly to stay aware of where your money is going. Awareness leads to better decisions and accountability.

Ask These Four Questions:

1. Which categories came in under budget? These are your wins. Note what made them work—a habit change, a meal planning decision, a canceled subscription.

2. Which categories ran over? For each one, identify whether it was a genuine one-off (a car repair, a doctor visit) or a pattern you underestimated. One-offs go into your sinking fund calculation. Patterns require adjusting next month’s budget target to reality.

3. Was the savings transfer maintained? If not, identify exactly what interrupted it and build a structural solution—earlier transfer date, different account setup, reduced amount that can actually be sustained.

4. What one thing would you change in month two? Pick one specific adjustment, not five. Compound small improvements over time rather than attempting wholesale overhauls that rarely hold.

5 Monthly Budget Mistakes Beginners Make

Understanding the most common mistakes helps you avoid them in your first budget.

Mistake 1—Budgeting From Gross Income Instead of Net

Using your salary instead of your actual take-home pay overstates your available income by 15–25%. A $60,000 salary is approximately $4,000 monthly take-home, not $5,000.

Mistake 2—Ignoring Sinking Funds for Irregular Expenses

Without monthly allocations for predictable annual expenses (car maintenance, insurance renewals, holiday gifts), each one arrives as a budget emergency. Sinking funds turn these into planned, manageable expenses.

Mistake 3—Not Tracking Weekly

Checking your budget only at month-end means discovering problems when it’s too late to adjust. Weekly 10-minute check-ins catch overspending while you can still course-correct.

Mistake 4—No Savings Automation

Hoping to save “what’s left over” at month-end rarely works. Automated transfers on payday—before discretionary spending begins—are how consistent savers actually save.

Mistake 5—No Buffer Category

Every realistic budget needs a $50–$150 miscellaneous line item for small unexpected expenses. Without it, a $40 parking fine or $60 plumber visit blows up your carefully planned categories.

The Monthly Budget Categories You Cannot Afford to Miss

Most budget guides cover the obvious categories. Here are the ones most first-time budgeters forget—and what happens when they do.

Irregular but Predictable Expenses—Sinking Funds

A budget can help anticipate expenses like car costs, utilities, or phone bills. The tool for this is a sinking fund—a small monthly allocation toward a known future expense.

| Forgotten Expense | Annual Cost | Monthly Sinking Fund |

|---|---|---|

| Car maintenance and tires | $900–$1,500 | $75–$125 |

| Annual insurance renewals | $400–$800 | $33–$67 |

| Medical deductibles and dental | $600–$1,200 | $50–$100 |

| Holiday gifts and travel | $800–$1,500 | $67–$125 |

| Home maintenance and repairs | $500–$2,000 | $42–$167 |

| Annual subscriptions (lump sum) | $200–$500 | $17–$42 |

| Birthday gifts and celebrations | $300–$600 | $25–$50 |

Without sinking funds for these, each one arrives as a budget emergency. With them, each one is already funded when it appears.

The Miscellaneous Buffer—The Category That Saves Your Budget

Every realistic monthly budget needs a miscellaneous line item of $50–$150 depending on income. Not because you plan to spend it on miscellaneous things—but because something always comes up that doesn’t fit neatly into any other category.

Budgets without a buffer break on the first $40 parking fine, the $25 emergency supply run, the $60 plumber visit for a slow drain. When a category exists for these, they are absorbed. When it doesn’t, they blow up a different category and the budget feels broken.

Monthly Budget Troubleshooting—The Most Common Problems Solved

Problem 1—”My needs alone exceed my income”

This is an income problem, not a budgeting problem. Budgeting cannot solve a mathematical deficit where genuine essential expenses exceed what arrives in your account. It can only make the gap visible.

Two routes forward: reduce fixed costs (move to a lower-rent area, refinance a car payment, negotiate a bill) or increase income.

For strategies on reducing expenses in difficult situations, read: How to Save Money on a Tight Budget

Problem 2—”I build the budget but stop checking it by week two”

The budget is the easy part. The habit of checking it is what most people struggle to maintain.

Fix: Reduce friction to the point of near-zero. If your tracking tool requires opening a laptop and loading a spreadsheet, it will lose the contest against your phone every time. Use a budgeting app that shows you your current status on your home screen. Set a weekly calendar reminder for Sunday evenings—ten minutes, not an hour.

Problem 3—”My partner and I can’t agree on the budget”

Research shows that about 50% of people across all age groups say unexpected expenses throw off their budgeting efforts—and when those unexpected expenses are contested between partners, the friction can derail the whole system.

The solution is not agreeing on every line item—it’s agreeing on the structure. Combined account for fixed shared expenses. Personal spending allocation for each partner, sized fairly relative to income. The shared budget only covers shared expenses. Personal budgets are each partner’s own business.

Full guide for couples: How to Budget as a Couple Without Fighting About Money

Problem 4—”I had a good month then blew the whole thing the next month”

This is the rebound pattern—the same psychology that produces yo-yo dieting produces yo-yo budgeting. A month of tight discipline followed by a month of relief spending that wipes out the progress.

Fix: Build wants spending into the budget deliberately. A budget that gives you $200 per month to spend on whatever you enjoy is not a compromise—it’s a sustainability mechanism. The 30% wants allocation in the 50/30/20 framework exists for this reason. Restriction that is 100% tight eventually breaks. Structured permission sustains.

Problem 5—”I don’t know what to do with money left over at the end of the month”

A surplus is the goal of the budget—and having a clear plan for it is what converts surplus into actual wealth rather than gradual lifestyle inflation.

Priority order for surplus: Emergency fund until three to six months of expenses are saved, then maximum employer retirement match, then high-interest debt above minimums, then medium-term saving goals, then investment accounts, then discretionary wants.

For everything about growing what you save: The Complete Guide to Personal Budgeting

Free Monthly Budget Template (Printable & Digital)

Copy this into any notes app, spreadsheet, or notebook. Fill it in at the start of each month.

MONTH: _______________

INCOME

Primary income (net): $______

Other income: $______

TOTAL INCOME: $______

SAVINGS FIRST

Emergency fund: $______

Retirement / investments: $______

Savings goal (name it): ______ $______

Extra debt repayment: $______

TOTAL SAVINGS: $______

FIXED NEEDS

Rent / mortgage: $______

Utilities (electric, gas, water):$______

Car payment: $______

Insurance (car, health, life): $______

Phone: $______

Internet: $______

Minimum debt payments: $______

Childcare / school: $______

TOTAL FIXED NEEDS: $______

VARIABLE NEEDS

Groceries: $______

Fuel / transport: $______

Medical / pharmacy: $______

TOTAL VARIABLE NEEDS: $______

WANTS

Dining out / delivery: $______

Entertainment: $______

Subscriptions (active ones): $______

Clothing / personal care: $______

Hobbies: $______

Miscellaneous buffer: $______

TOTAL WANTS: $______

SINKING FUNDS

Car maintenance: $______

Annual expenses: $______

Gifts / celebrations: $______

TOTAL SINKING FUNDS: $______

FINAL CHECK

Total Income: $______

Total All Categories: - $______

BALANCE (should be zero = $______

or positive):For a ready-to-use digital version of this monthly budget template: Best Free Budget Spreadsheet Templates

Real People, Real First Budgets—What Actually Happened

Kenji, 27—Graphic Designer, Seattle

Kenji had tried to budget twice before. Both times he built it, tracked it for two weeks, and stopped. The third attempt was different for one reason: he connected the budget to a specific goal—saving $8,000 for a three-week trip to Japan in fourteen months.

He built his first complete monthly budget in 45 minutes using the steps above. He found $290 per month in subscriptions he had forgotten about and $340 per month in food delivery he had genuinely underestimated. He canceled the subscriptions, reduced delivery to Fridays only, and put $600 per month toward his Japan fund.

Fourteen months later: $8,400 saved. He took the trip. His budget survived because it was pointed at something real.

“The difference between the budgets that failed and the one that worked was having a destination. The spreadsheet was the same. The goal changed everything.”

Amara, 33—NHS Nurse, Birmingham, UK

Amara’s challenge was irregular shifts—her take-home varied by £300–£500 month to month depending on overtime. She had avoided budgeting because she assumed it required stable income.

She built her budget from her three lowest-earning months’ average—£2,100 take-home. Any income above that in higher months went first to her emergency fund, then to her ISA.

Four months in: Emergency fund at £2,800—the first financial buffer she had ever had. She had also discovered she was spending £180 per month on food delivery on overnight shift nights. She started batch cooking before night rotations. Monthly saving: £140.

“I thought budgeting was for people with predictable salaries. It actually works better for irregular income because it removes the anxiety of not knowing whether you’ll be okay in a lower month.”

Frequently Asked Questions

How do I make a monthly budget for the first time if I have never tracked my spending?

To make a monthly budget for the first time, start with three months of bank and credit card statements rather than relying on memory. Open every account you use—including any payment platforms—and categorize every transaction. This takes 60–90 minutes the first time and gives you real averages rather than estimates. Build your first budget from those real numbers, not from what you hope you spend. Creating a monthly budget from scratch may seem intimidating, but building a personal budget is one of the most powerful steps you can take toward financial stability and long-term success.

What are the most important categories in a monthly budget?

Every complete monthly budget needs six types of categories: fixed needs (rent, insurance, minimum debt payments), variable needs (groceries, fuel, utilities), savings (emergency fund, retirement, goals), wants (dining, entertainment, hobbies), sinking funds (irregular predictable expenses like car maintenance and annual bills), and a miscellaneous buffer. Most first budgets fail because they include the first two categories and skip the rest—particularly sinking funds and a buffer, which are what prevent budget emergencies from blowing up an otherwise working plan.

How long does it take to make a monthly budget from scratch?

The first budget takes 60–90 minutes if you gather your statements beforehand. Subsequent monthly budgets—updating from the previous month’s template—take 20–30 minutes. The ongoing weekly check-in takes 10 minutes. The investment of time in the first month is the setup cost for a system that then runs with minimal ongoing effort.

What should I do if my expenses are higher than my income when I build my budget?

A deficit revealed by the budget is not the budget failing—it’s the budget working. It has made a real problem visible rather than letting it accumulate silently. If you’re spending more than you earn, you’ll need to make cuts—starting with variable expenses or reviewing unnecessary fixed costs like unused subscriptions. Begin with the easiest cuts—forgotten subscriptions, reduced food delivery—before tackling fixed costs which require more significant changes. If cuts alone cannot close the gap, the other side of the equation needs attention alongside the budget. Read our guide on how to save money fast for specific tactics.

How often should I update my monthly budget?

Build a fresh budget at the start of each month—it takes 20–30 minutes and accounts for anything changing from the previous month. Review it against actual spending once per week. Do a deeper review every three to six months to assess whether your savings targets, wants allocations, and overall structure still match your current situation and goals. A budget built in February will not perfectly fit October if your life has changed in between.

What’s the difference between a monthly budget and the 50/30/20 rule?

A monthly budget is a comprehensive plan that allocates all income across specific expense and savings categories. The 50/30/20 rule is a specific budgeting method that divides income into three percentage-based buckets: 50% needs, 30% wants, 20% savings. You can build a monthly budget that follows the 50/30/20 structure, or use a more detailed approach like zero-based budgeting. The best method depends on your income stability, housing costs, and financial goals.

Should I use a budgeting app or a spreadsheet?

The best tool is the one you’ll actually use consistently. Research shows that 27% of young adults prefer budgeting apps, 39% of middle-aged adults favor spreadsheets, and 43% of older adults use pen and paper. Apps like Monarch, YNAB, and Rocket Money offer automatic bank syncing and real-time tracking. Spreadsheets provide complete customization and cost nothing. For a complete comparison, see our guide to the best budgeting apps or download our free budget spreadsheet templates.

Sources

All steps, categories, and recommendations in this guide are sourced from the following verified sources:

- Bankrate How to Make a Monthly Budget August 2025

- WalletHub Budgeting Statistics 2025

- Debt.com Annual Budgeting Survey 2025

- Moneywise Personal Finance Statistics 2025

- InCharge How to Create a Budget 2025

- Finkerr How to Create a Monthly Budget 2025

- CNBC Select How to Create a Budget 2025

- Microsoft 365 Budgeting Tips 2024

- Consumer Financial Protection Bureau Making Ends Meet 2024

- National Endowment for Financial Education Financial Well-Being Survey 2025

- Federal Reserve Survey of Consumer Finances 2024

- Bureau of Labor Statistics Consumer Expenditure Survey 2023

Ready to build your first budget? Start with this guide, then explore our complete personal budgeting framework to understand which budgeting method fits your situation best. For automatic tracking, see our guide to the best budgeting apps, or download our free monthly budget template to get started immediately.