Jessica earns $4,200 take-home per month. She found the 50/30/20 rule on a Monday, built her first budget by Tuesday, and felt genuinely organized about money for the first time in three years.

By Thursday she was confused. Her rent alone was $1,600. That’s 38% of her income before groceries, transport, insurance, or her phone bill had been touched. By the time she tallied her actual essential expenses, she was at 63%—not 50%. The framework seemed broken before it had started.

She’s not alone. This exact experience—excitement about a simple system followed by the sinking realization that the numbers don’t match reality—is the most common reason people abandon the 50/30/20 rule within a week of discovering it.

Here’s the thing: the rule isn’t broken. But it’s also not complete as most articles describe it.

This guide explains exactly how the 50/30/20 rule works, where it genuinely works well, where it honestly falls short, and—most importantly—what to do when your real numbers don’t fit the framework. Real income examples. Real adjustments. No oversimplification.

Table of Contents

What Is the 50/30/20 Rule?

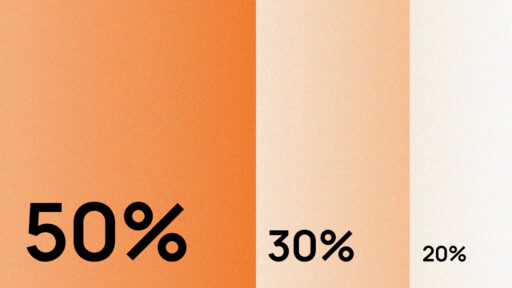

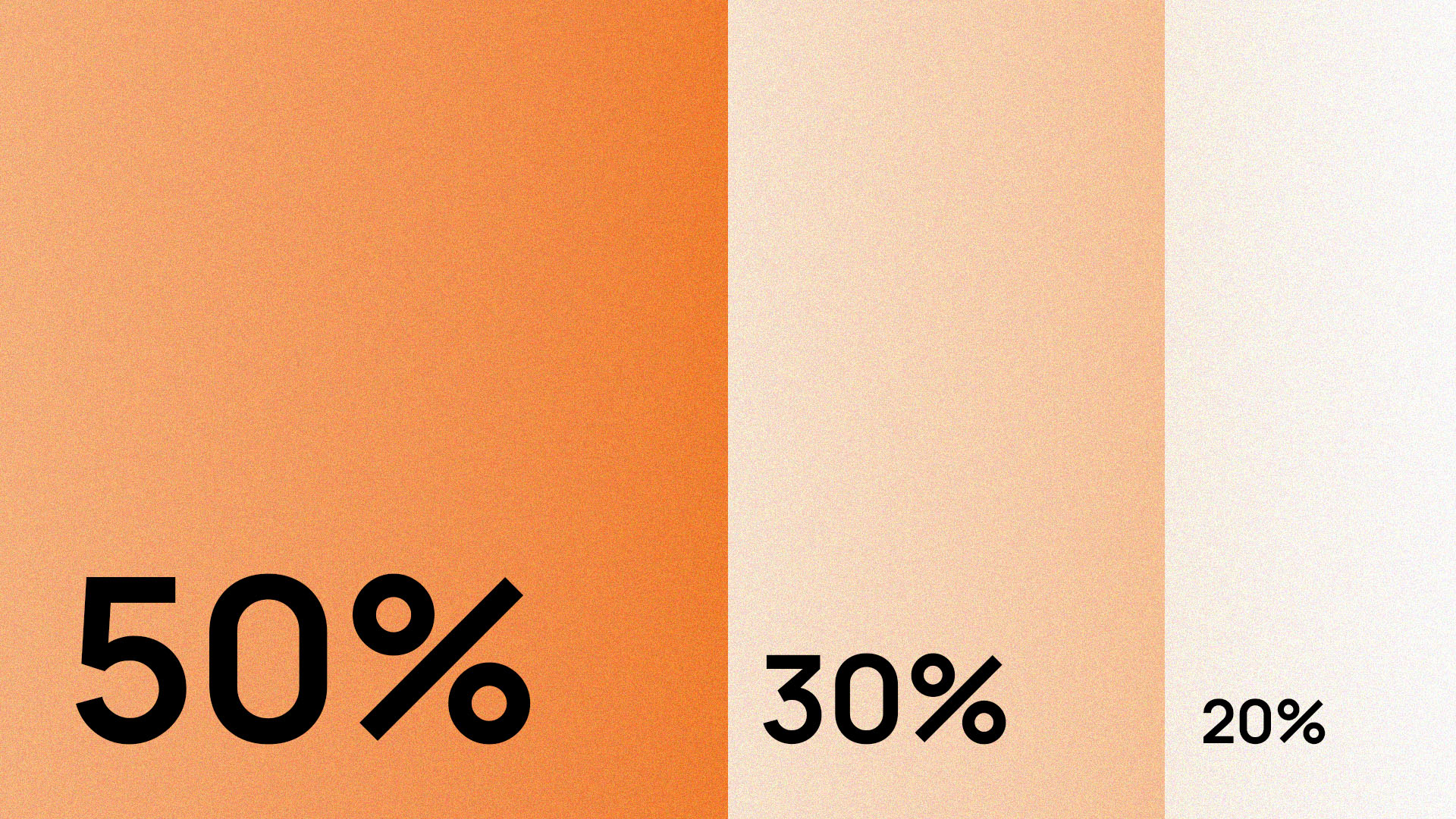

The 50/30/20 rule is a budgeting method that divides your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Created by US Senator Elizabeth Warren, it provides a simple framework for managing money without tracking dozens of spending categories.

Where the 50/30/20 Rule Came From

The 50/30/20 budget rule was popularized by US Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, which she co-wrote with her daughter Amelia Warren Tyagi. The original goal was a budgeting system that was simple, sustainable, and rooted in how real households actually spend money rather than how financial advisors wish they would.

Warren was a bankruptcy law professor before her political career. Her research into why ordinary American families ended up in financial crisis consistently pointed to one structural failure: they had no framework for how their income should be proportioned. They weren’t reckless. They were unstructured. The 50/30/20 rule was her answer to that—a framework simple enough that any household could apply it within an hour, without a finance degree or a spreadsheet.

The core idea: 50% of your money goes toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you’ll need to realize your future goals.

Three numbers. No complex category tracking. No forty-line spreadsheet. Just a framework for understanding whether your income is being proportioned in a way that leaves room for both your present life and your financial future.

For a complete overview of how this method compares to other budgeting approaches, see our complete guide to personal budgeting.

How the 50/30/20 Budget Rule Works — The Three Buckets Explained

The 50% Bucket — Needs

About half of your budget should go toward needs—expenses that must be met no matter what.

What genuinely belongs here: rent or mortgage, utilities, groceries, transport (car payment, fuel, insurance, public transport), health insurance, phone (basic plan), minimum debt payments, and childcare if applicable.

The test for whether something is a need: Could you lose your job, your housing, or your health without it? If yes—need. If no—want.

The grey areas are where most people get confused:

| Expense | Need or Want? | Why |

|---|---|---|

| Basic internet at home | Need | Required for job applications, remote work, healthcare access |

| Streaming service | Want | You’d survive without Netflix |

| Groceries | Need | Food is non-negotiable |

| Dining out | Want | The food is optional—cooking at home is the need alternative |

| Basic phone plan | Need | Communication is essential |

| Latest iPhone upgrade | Want | The communication function doesn’t require the upgrade |

| Minimum credit card payment | Need | Avoiding default is non-negotiable |

| Extra credit card payment | Savings bucket | Paying beyond minimum is a financial goal |

| Car insurance | Need | Legal requirement in most states |

| Gym membership | Want | Exercise can happen without a gym |

The strict rule: If you can honestly say “I cannot function without this,” it’s a need. If you would survive without it, it’s a want.

The 30% Bucket — Wants

The wants bucket is your guilt-free spending money—dining out, shopping, subscriptions, travel, and entertainment.

Ever wonder how much spending money you should have each month? The 50/30/20 budget rule gives you 30% to spend however you like, which might be more sustainable than ultra-restrictive plans.

This is intentionally generous, and that’s the point. Budgets that allow zero discretionary spending fail because nobody maintains zero indefinitely. The 30% wants allocation creates room for a real life within the budget—for the dinner out that matters, the holiday that recharges you, the hobby that keeps you sane. It just puts a number on it rather than letting it expand without limit.

The 20% Bucket — Savings and Goals

The final bucket is dedicated to goals. Financial goals vary between individuals—many people choose to allocate a percentage of their take-home pay toward savings and debt payoff goals.

This 20% is doing the work that determines your financial future. It covers emergency fund contributions, retirement savings (401k, IRA, pension), investing, extra debt repayment beyond minimums, and saving toward specific goals like a house deposit.

The critical distinction from the needs bucket: Minimum debt payments belong in needs because they’re non-negotiable obligations. Extra debt repayment belongs here because it’s a deliberate choice to pay faster than required—a financial goal, not a survival requirement.

For guidance on what to do with this 20% first, read our guide on how to build an emergency fund from zero.

50/30/20 Rule Example — Real Income Scenarios

The percentages in the 50/30/20 budget can be changed to fit your financial needs at a given moment. But before adjusting, it helps to see what the standard framework looks like at different income levels.

| Take-Home Pay (Monthly) | Needs (50%) | Wants (30%) | Savings (20%) | Annual Savings Built |

|---|---|---|---|---|

| $2,500 | $1,250 | $750 | $500 | $6,000/year |

| $3,500 | $1,750 | $1,050 | $700 | $8,400/year |

| $4,200 | $2,100 | $1,260 | $840 | $10,080/year |

| $5,000 | $2,500 | $1,500 | $1,000 | $12,000/year |

| $7,000 | $3,500 | $2,100 | $1,400 | $16,800/year |

These figures use after-tax take-home pay—not gross salary. Always calculate from what actually lands in your account.

Is the 50/30/20 Rule Realistic in 2026?

The answer depends entirely on what “work” means and whether the framework fits your actual numbers.

Where the 50/30/20 Rule Genuinely Works

Many budgeting systems fail because they demand too much precision. The 50/30/20 budget rule focuses on habits and direction rather than perfection.

For people with moderate incomes, stable monthly expenses, and no extreme debt load in a mid-cost-of-living area, the 50/30/20 rule works exactly as described. It’s the simplest budgeting method available. It takes 20–30 minutes to apply. It requires no ongoing category-by-category tracking. And it consistently produces better financial outcomes than having no framework at all—which is the actual alternative for most people who abandon complex budgets.

According to the US Consumer Financial Protection Bureau, this balanced approach simplifies budgeting and helps users avoid overspending in any one area.

Where the 50/30/20 Rule Honestly Falls Short

High cost of living areas: The 50/30/20 budget rule can be a good budgeting method for some, but it may not work for your unique monthly expenses. Depending on your income and where you live, earmarking 50% of your income for your needs may not be enough.

In cities like New York, San Francisco, London, or Sydney, rent alone frequently consumes 40–50% of take-home pay for median earners—before utilities, food, transport, or insurance. The 50% needs allocation simply doesn’t accommodate the actual cost structure of these housing markets.

Low-income households: When total income barely covers essential expenses, the 30% wants allocation is a mathematical impossibility and the 20% savings allocation feels like a cruel joke. For households where needs genuinely consume 70–80% of income, the framework needs restructuring rather than application.

High debt loads: Someone carrying $40,000 in student debt, $8,000 in credit card debt, and a car payment is not going to make meaningful debt progress from 20% of a moderate income. They likely need to temporarily compress the wants bucket and redirect that allocation toward accelerated debt repayment.

Irregular income: Freelancers, gig workers, commission-based earners, and small business owners cannot apply fixed percentages to income that fluctuates by $1,000–$3,000 month to month without building in significant buffers.

Does the 50/30/20 Rule Work in Expensive Cities?

For residents of high-cost cities, the standard 50/30/20 budget rule requires significant adjustment before it applies.

New York City: Median one-bedroom rent in Manhattan is approximately $4,200/month. On a $75,000 salary ($4,700 take-home), that’s 89% of income before any other expense.

San Francisco: Average rent for a one-bedroom is $3,400/month. On a $80,000 salary ($5,000 take-home), that’s 68% of income.

London: Average rent in Zone 2 is approximately £2,100/month. On a £45,000 salary (£2,900 take-home), that’s 72% of income.

Sydney: Median one-bedroom rent is approximately AUD $2,800/month. On a AUD $70,000 salary (AUD $4,500 take-home), that’s 62% of income.

The adjustment for expensive cities: Compress wants to 15–20% and reduce savings to 10–15% temporarily while working on either reducing housing costs (roommates, living further out) or increasing income. The 50/30/20 framework becomes more like 65/15/20 or 60/20/20 until housing costs can be brought down.

For strategies on reducing expenses in expensive cities, see our guide on how to save money on a tight budget.

The Real-World Test — What Happens When You Run the Numbers

Here’s the exercise most articles skip. Before deciding whether the 50/30/20 rule works for you, run your own numbers honestly.

Step One — Calculate Real Take-Home Pay

Look at your last two payslips. Use the net figure—what deposits after tax and deductions. If income varies, use a conservative three-month average.

Step Two — List Every Essential Expense and Total Them

| Essential Expense | Your Monthly Amount |

|---|---|

| Rent or mortgage | $ |

| Utilities (electricity, gas, water) | $ |

| Groceries | $ |

| Transport (car payment, fuel, insurance, transit) | $ |

| Health insurance (employee portion) | $ |

| Phone (basic plan) | $ |

| Minimum debt payments | $ |

| Childcare (if applicable) | $ |

| Total Needs | $ |

Step Three — Divide Total Needs by Take-Home Pay

If your total needs are $1,900 on a $3,500 take-home, that’s 54%—slightly over. Adjustable.

If your total needs are $2,800 on a $3,500 take-home, that’s 80%—the framework needs restructuring before it applies.

The result tells you which version of the rule fits your situation.

How to Calculate the 50/30/20 Rule

The 50/30/20 calculator formula is simple:

Take-home pay × 0.50 = Needs budget

Take-home pay × 0.30 = Wants budget

Take-home pay × 0.20 = Savings budget

50/30/20 Calculator Example:

Monthly take-home: $4,000

- $4,000 × 0.50 = $2,000 (Needs)

- $4,000 × 0.30 = $1,200 (Wants)

- $4,000 × 0.20 = $800 (Savings)

Monthly take-home: $5,500

- $5,500 × 0.50 = $2,750 (Needs)

- $5,500 × 0.30 = $1,650 (Wants)

- $5,500 × 0.20 = $1,100 (Savings)

Monthly take-home: $3,000

- $3,000 × 0.50 = $1,500 (Needs)

- $3,000 × 0.30 = $900 (Wants)

- $3,000 × 0.20 = $600 (Savings)

Use your actual take-home pay in these calculations, not your gross salary. This is your take-home pay, not your salary.

What If My Needs Are More Than 50%?

For many people, especially in high-cost areas, needs may exceed 50% temporarily. When this happens, the adjustment framework is straightforward:

The rule to follow: Compress Wants before touching Savings.

If saving or paying down debt is a priority, it’s fine to shrink your wants bucket and increase the savings and debt bucket. The same logic applies in reverse—if needs are unavoidably high, reduce wants first.

| Needs % | Recommended Adjustment |

|---|---|

| 50–55% | Reduce wants to 25%, keep savings at 20% |

| 55–65% | Reduce wants to 20%, keep savings at 15–20% |

| 65–75% | Reduce wants to 10–15%, savings at 10–15% |

| Above 75% | Standard framework doesn’t apply—use zero-based budgeting instead |

The minimum to protect regardless of needs: Keep at least 10% going to savings. Even $200–$300 per month builds an emergency fund and retirement contributions. Dropping savings to zero because needs are high is the choice that makes everything harder long-term.

When Your Numbers Don’t Fit — The Adjustment Framework

The percentages are guidelines, not requirements. Here are the specific adjustments for the most common situations where the standard framework doesn’t fit.

Adjustment 1 — When Needs Exceed 50%

See the table above for specific adjustments based on your needs percentage.

For practical tactics on reducing your needs and wants categories, read our guide on how to save money fast.

Adjustment 2 — When You Have Significant Debt

If you’re carrying high-interest debt—credit cards, personal loans above 10% interest—temporarily restructure to something closer to 50/20/30, where the last 30% is split between wants and accelerated debt repayment rather than the standard 30% wants allocation.

You may remember that debts are a part of the needs category as well—minimum required payments belong there. If you plan to pay down debt sooner, the excess amount you put toward that debt would be included in your goals bucket.

A practical debt-focused variation:

| Bucket | Standard 50/30/20 | Debt-Priority Variation |

|---|---|---|

| Needs | 50% | 50% |

| Wants | 30% | 15% |

| Savings | 10% | 10% |

| Extra debt repayment | 10% (within savings) | 25% |

Once high-interest debt is eliminated, return to the standard framework—with the same income now producing significantly more discretionary room.

Adjustment 3 — When Income Is Irregular

Rather than applying percentages to monthly income—which fluctuates—apply them to your conservative baseline income. Calculate your average income across your three lowest-earning months in the past year. Budget from that number. Any income above that baseline in higher-earning months goes entirely to savings and emergency fund first, then wants second.

This protects you from building a lifestyle on peak income that becomes unsustainable during slow months.

50/30/20 vs Zero-Based Budgeting — Comparison

If the 50/30/20 method doesn’t fit your lifestyle, other methods include the envelope system—which works well for people who want to curb impulse purchases and feel more emotionally connected to their money—and zero-based budgeting, geared toward people who want to assign a job to every dollar until they have zero dollars left unassigned at the end of the month.

| Method | Setup Time | Best For | Biggest Weakness |

|---|---|---|---|

| 50/30/20 Rule | 20–30 mins | Beginners, simple structure | Doesn’t work for high-cost-of-living |

| Zero-Based Budget | 60–90 mins/month | Specific goals, maximum control | Irregular income makes it unstable |

| Envelope System | 30 mins | Overspenders needing hard limits | Less flexible for digital spending |

| Pay Yourself First | 15 mins | Non-trackers, automation lovers | Less insight into category spending |

| Two-Account System | 20 mins | Couples, casual budgeters | Misses investment opportunities |

For most beginners: start with the 50/30/20 rule to build the habit. Once the habit is established—typically after 3–4 months—assess whether more granular control (zero-based) or more automation (pay yourself first) would serve your goals better.

For a complete comparison of all budgeting methods, see our complete guide to personal budgeting.

For a deep dive into zero-based budgeting specifically, read our zero-based budgeting guide.

Real People Using the 50/30/20 Rule — What Happened

Priya, 26 — Freelance Designer, London

Priya’s income ranged from £2,800 to £4,400 per month depending on client workload. She budgeted from a conservative baseline of £3,000.

Her first month applying the 50/30/20 rule: needs came to 58% of her baseline. She compressed wants to 22% and kept savings at 20%. When she earned above baseline, the additional income went directly to savings.

Six months later: £6,400 saved. Her high-earning months had been building her emergency fund quietly for half a year.

“The rule didn’t work perfectly off the shelf. I had to adjust it. But the structure of three buckets—rather than forty categories—was what made it sustainable for someone with irregular income.”

David and Claire, 31 and 33 — Dual Income, Chicago

Combined take-home: $8,200/month. They had been “sort of budgeting” for two years with no consistent method and no measurable progress on savings.

Their needs calculation: $4,600 (56%—housing in Chicago pushed it over). They adjusted to 56/24/20—needs at 56%, wants compressed to 24%, savings protected at 20%.

Twelve months later: $19,680 in savings. First time either of them had felt financially organized as a couple.

“The specific percentages mattered less than having an agreed-upon framework we both understood and checked together. That monthly conversation about money was completely new for us.”

For budgeting as a couple specifically, read: How to Budget as a Couple Without Fighting About Money

How to Start the 50/30/20 Rule This Week — Step by Step

Step 1 — Calculate Your Real Take-Home Income

Look at your last two payslips. Use the net figure—what deposits after tax and deductions. If income varies, use a conservative three-month average.

Step 2 — Apply the Percentages to Get Your Target Buckets

Multiply your take-home by 0.50, 0.30, and 0.20. Write these three numbers down. They’re your targets—not your constraints.

Step 3 — Total Your Actual Essential Expenses

Use real statements, not memory. Every fixed essential expense, totalled honestly. Compare to your 50% target.

Step 4 — Identify Your Adjustment

If actual needs are within 5% of the 50% target—the standard framework applies directly. If needs exceed 50% significantly, apply the adjustments above before proceeding.

Step 5 — Set Up the Savings Transfer Automatically

Before spending from your wants bucket, automate the savings transfer. On payday, $X moves to your savings or investment account without a decision being made. This is non-negotiable—the 50/30/20 framework encourages saving and debt repayment, contributing to long-term financial stability. That contribution has to happen before discretionary spending, not after.

Where to put the savings: Read our guides on how to build an emergency fund from zero and how to save money fast.

Step 6 — Track Spending Weekly for the First Month

For the first 30 days, check your spending against your three buckets once per week. Not daily—weekly. The goal is awareness of which bucket is running ahead, not obsessive monitoring.

The best tools for tracking: Best Budgeting Apps That Actually Change Your Money

For a complete step-by-step system, read our guide on how to create a monthly budget from scratch.

50/30/20 Rule — Pros and Cons

Understanding both the strengths and limitations of the 50/30/20 budget rule helps you decide if it’s the right framework for your situation.

Pros:

- Simple structure — Three numbers instead of tracking dozens of categories

- Easy to apply — Takes 20–30 minutes to set up initially

- Sustainable for beginners — Low maintenance compared to complex budgeting systems

- Encourages consistent saving — The 20% savings allocation is built into the framework

- Flexible enough to adjust — Percentages can be modified for different life situations

- Prevents lifestyle inflation — Caps discretionary spending at 30% regardless of income growth

Cons:

- Doesn’t work in high-cost cities — Housing costs often exceed 50% of income alone

- Too rigid for irregular income — Fixed percentages don’t accommodate fluctuating earnings

- Not detailed enough for aggressive goals — Lacks the granularity needed for rapid debt payoff or aggressive saving

- Assumes stable employment — Doesn’t account for job loss, medical emergencies, or major life changes

- No guidance on investment allocation — Doesn’t specify how to use the 20% savings bucket

- Can oversimplify complex situations — High debt loads or multiple financial priorities need more nuanced approaches

The Six Most Common 50/30/20 Mistakes — And How to Fix Each One

Mistake 1 — Using Gross Income Instead of Take-Home Pay

This is your take-home pay, not your salary. A $60,000 salary is roughly $4,000–$4,300 monthly take-home after federal and state taxes, not $5,000. Budgeting from gross salary makes every bucket 15–20% larger than it actually is.

Mistake 2 — Calling Subscriptions and Habits “Needs”

Expenses like streaming subscriptions or premium services are often labeled as needs when they’re wants. Be ruthless with the categorization. A subscription is a want. Groceries are a need. These are different things.

Mistake 3 — Skipping the Savings Transfer and Hoping Something Is Left

The rule specifies 20% to savings. That means it leaves your account on payday, automatically, before your wants bucket is touched. The reverse—spending first and saving what remains—is how 69% of Americans end up paycheck to paycheck despite having budgets.

Mistake 4 — Not Adjusting When Life Changes

Revisit your budget every few months to make sure it still fits your goals and life circumstances, and make adjustments as necessary. Got a raise? Increase the savings percentage before increasing lifestyle. Lost income? Compress wants immediately rather than letting needs creep or savings disappear.

Mistake 5 — Treating the Percentages as Absolute

The 50/30/20 rule works best as a guiding structure rather than a strict formula. A month where you spend 55% on needs and 15% on wants is not a failure—it’s a normal month with a car repair or a medical bill. Adjust the following month rather than abandoning the system.

Mistake 6 — No Specific Goal Attached to the 20%

Money directed toward “savings” with no purpose tends to migrate back to spending within a few months. Name your 20%—emergency fund until three months is reached, then retirement contributions, then house deposit fund. Specific named goals are significantly harder to raid than unnamed savings accounts.

For strategies on turning vague savings goals into concrete action, read our emergency fund guide.

What the 50/30/20 Rule Does Not Cover

Being honest about the limits of any framework is what makes it genuinely useful rather than just promotional.

The 50/30/20 rule doesn’t tell you how to invest your savings once you have them. It doesn’t address which debts to pay off first. It doesn’t help you choose between a pension contribution and an ISA or Roth IRA. It doesn’t account for major life changes like having a first child or losing a job.

For all of those questions, it’s a starting framework that needs supplementing with specific knowledge.

Read next:

- How to Build an Emergency Fund From Zero — what to do with your 20% first

- How to Save Money Fast — practical tactics for getting your needs and wants buckets under control

- The Complete Guide to Personal Budgeting — the full framework this rule fits within

- Best Budgeting Apps — tools to track your 50/30/20 split automatically

- How to Budget as a Couple — applying the 50/30/20 rule with a partner

Frequently Asked Questions

What is the 50/30/20 rule in simple terms?

The 50/30/20 rule is a budgeting method that recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. It’s applied to your after-tax take-home pay—not your gross salary. The simplicity is the point: three numbers instead of forty categories, applied to everything you earn.

Is the 50/30/20 rule realistic in 2026?

The 50/30/20 rule is realistic for people with moderate incomes in mid-cost-of-living areas. However, it may not work for your unique monthly expenses depending on your income and where you live—earmarking 50% of your income for your needs may not be enough. In high-cost cities or for people with significant debt loads, the standard percentages need adjustment before the framework applies. The rule is a starting point, not a final answer. For complete guidance on building a budget that fits your situation, see our personal budgeting guide.

What counts as a “need” in the 50/30/20 rule?

Needs are expenses that must be met no matter what—if you can honestly say “I cannot live without it,” you’ve identified a need. This includes housing, utilities, groceries, transport, insurance, minimum debt payments, and childcare. It doesn’t include streaming services, gym memberships, dining out, or subscriptions—those are wants regardless of how habitual they’ve become.

What if my needs already take up more than 50% of my income?

For many people, especially in high-cost areas, needs may exceed 50% temporarily. The adjustment is to compress the wants bucket first—reduce discretionary spending to 20–25% rather than 30%—while protecting the savings allocation as much as possible. Only reduce savings below 15% as a last resort, and treat that as a temporary state while you work on either reducing fixed costs or increasing income. For specific strategies, read our guide on saving money on a tight budget.

Does the 50/30/20 rule include investing?

Yes. The 20% portion can include investing, saving, or debt repayment. Within the savings bucket, the recommended priority is: emergency fund first (until you have three months of expenses), then employer retirement match contributions, then additional investing, then saving toward specific medium-term goals. Read our emergency fund guide to understand where to start.

How is the 50/30/20 rule different from zero-based budgeting?

The 50/30/20 rule allocates by percentage across three broad buckets—high-level guidance, low ongoing effort. Zero-based budgeting assigns a specific purpose to every dollar across detailed categories until the month’s income minus all assignments equals zero. Zero-based budgeting gives more control and works better for specific aggressive savings goals or debt elimination. The 50/30/20 rule works better for people who want structure without micromanagement. The choice depends on personality, income stability, and financial goals. For a complete comparison, read our zero-based budgeting guide.

Can I use the 50/30/20 rule with irregular income?

Yes, but you need to modify the approach. Calculate your average income across your three lowest-earning months in the past year and budget from that conservative baseline. Apply the 50/30/20 percentages to that number. Any income above baseline in higher-earning months goes entirely to savings first, then wants second. This prevents building a lifestyle on peak income that becomes unsustainable during slow months.

How do I track my spending with the 50/30/20 rule?

The simplest method is to review your bank and credit card statements weekly during your first month to ensure you’re staying within each bucket’s allocation. Many budgeting apps can automatically categorize your spending and show you where you stand against your 50/30/20 targets. Alternatively, you can use free budget spreadsheet templates for manual tracking with full control.

Sources

All data, percentages, and recommendations in this guide are sourced from the following verified sources:

- Elizabeth Warren — All Your Worth: The Ultimate Lifetime Money Plan

- NerdWallet 50/30/20 Budget Calculator January 2026

- LendEDU What Is the 50/30/20 Rule January 2026

- Chase Bank 50/30/20 Rule Explained

- Citizens Bank 50/30/20 Budget March 2025

- SAFE Federal Credit Union Budgeting Rule Guide

- John Hancock Debunking the 50/30/20 Rule

- Gotrade 50/30/20 Rule Explained February 2026

- US Consumer Financial Protection Bureau Budgeting Guidance

- National Endowment for Financial Education Research

- Bureau of Labor Statistics Consumer Expenditure Survey 2023

- Federal Reserve Survey of Consumer Finances 2024

Ready to put the 50/30/20 rule into action? Start with our step-by-step guide to creating a monthly budget, then use the best budgeting apps to track your progress automatically. For additional money-saving strategies to help you stay within your 30% wants allocation, see our guide on how to save money fast.