Quick Summary: Personal Budgeting Guide (2026)

What this guide covers:

- How to build a realistic monthly budget in under 90 minutes using your actual spending data

- The 5 most effective budgeting methods (50/30/20, zero-based, envelope system, pay yourself first, two-account system) — with honest pros and limitations

- Recommended budget allocations: 25–35% housing, 10–20% savings, 10–15% food and transportation

- The three core reasons most budgets fail — and how to avoid them

- The best budgeting tools and apps for different personality types

Key Insight:

Nearly 69% of Americans live paycheck to paycheck, yet most say they already budget. The issue isn’t having a budget — it’s having one built on unrealistic assumptions. This guide shows you how to build a system based on your real numbers, not ideal targets.

Time Required:

60–90 minutes to set up. 10 minutes per week to maintain.

Best For:

• Beginners who want clarity

• People who have tried budgeting and quit

• Couples managing money together

• Anyone serious about breaking the paycheck-to-paycheck cycle

Table of Contents

What is Personal Budgeting?

Personal budgeting is a forward-looking financial plan that allocates income toward expenses, savings, and debt repayment before money is spent.

Before diving into methods and tactics, let’s clear something up.

Personal budgeting is not a spreadsheet that tells you what you spent last month. That’s expense tracking. Useful—but not a budget.

Personal budgeting is a plan that tells your money where to go before it leaves your account. The key word is before. A real budget is made at the start of the month or the pay period, not assembled afterward from receipts.

It’s also not a punishment. It’s not a document that catalogues everything you’re not allowed to enjoy. The budgets that fail—the ones that last three weeks before being quietly abandoned—are almost always built around restriction rather than intention.

The budgets that work are built around permission. You decide deliberately what matters to you. You fund those things first. Then you see what’s left and allocate it accordingly.

That distinction—restriction versus intention—is the difference between budgets people maintain and budgets people quit.

Why Personal Budgeting Matters More in 2026 Than Ever Before

Essential expenses—groceries, utilities, insurance, healthcare, auto costs, gas, home maintenance, and telephone—totaled roughly $4,000 per month for the average American household in 2025. That’s before rent. Before entertainment. Before anything discretionary.

Recent survey data shows that saving money is the top New Year’s resolution for 2026—edging out other common resolutions like eating healthier, exercising, and losing weight. People know they need to do something. Most don’t know specifically what.

Fewer than 43% of Americans consider themselves financially secure. In 2024, 44% of consumers felt their finances “control their life” always or often.

A personal budget doesn’t solve all of that. But it’s the foundation beneath everything else—the framework that makes saving possible, debt repayment structured, and financial goals achievable rather than theoretical.

Among people who do budget, over 84% report that it has helped them either avoid debt or pay it off. Nearly 95% say budgeting is now more important than ever.

The evidence isn’t ambiguous. A working personal budget changes financial outcomes. The question is how to build one that actually works for your life.

The Real Reason Most Budgets Fail

According to financial surveys, 74% of people who budget say that increasing costs are the biggest challenge they face when trying to stick to their budget. That’s a real and fair point. But it doesn’t explain why people with stable incomes also abandon their budgets.

The deeper reason is misalignment—the budget was built around a theory of what someone should want to spend money on, rather than what they actually do.

A budget that gives you $200 per month for dining out when you genuinely value and regularly spend $400 on food experiences isn’t a realistic budget. It’s an aspiration disguised as a plan. Aspirations fail by month two. Plans built on reality last.

The second reason is the tracking burden. Research shows that higher-income individuals prefer spreadsheets (45%) while low-income individuals rely more on pen and paper (49%) or apps (23%). The tool matters less than the habit. Any tracking system that feels onerous gets abandoned. The best budget system is the one you’ll actually use.

The third reason—the one almost nobody talks about—is no clear connection to a goal. A budget built in service of nothing is just a list of numbers. A budget built to fund a house deposit, or to become debt-free by a specific date, or to reach a first month of full emergency fund—that budget has a reason to exist every time you check it.

How to Create Your First Budget: Step-by-Step Guide

Every personal budget starts with two honest figures. Most people skip the honesty part.

Step 1: Calculate Your Real Monthly Income

Write down your actual take-home pay after taxes and deductions. Not your salary. Not what you wish you earned. What lands in your account each month.

If your income is irregular—freelance, commission-based, seasonal—calculate a conservative average using your three lowest months in the past twelve. Always budget from the floor, not the ceiling, of your income.

Income Worksheet:

| Income Source | Monthly Amount (After Tax) |

|---|---|

| Primary job/salary | $ |

| Side income/freelance | $ |

| Other regular income | $ |

| Total Take-Home Income | $ |

Step 2: Track Your Real Monthly Expenses

This step requires looking at actual statements—not estimating from memory. According to the Bureau of Labor Statistics, the average American household spent $77,280 in 2023, a 51% increase from 2013. Most people underestimate their monthly spending by $200–$400 because memory consistently underweights small, frequent purchases.

Open three months of bank statements and credit card statements. Categorize every transaction. Total each category. Then average across the three months.

Expense Worksheet:

| Category | Your Monthly Average |

|---|---|

| Housing (rent/mortgage) | $ |

| Utilities (electricity, gas, water) | $ |

| Groceries | $ |

| Transport (fuel, insurance, car payment) | $ |

| Phone and internet | $ |

| Insurance (health, life, renters/homeowners) | $ |

| Subscriptions (streaming, apps, memberships) | $ |

| Dining out and food delivery | $ |

| Entertainment | $ |

| Clothing | $ |

| Personal care | $ |

| Minimum debt payments | $ |

| Everything else | $ |

| Total Monthly Expenses | $ |

The difference between your total income and total expenses is your current monthly surplus or deficit. That number—however uncomfortable—is your starting point.

Step 3: Choose a Budgeting Method

This is the decision most guides skip by recommending one method as universally best. There is no universally best method. There is only the method that fits how your brain naturally relates to money.

See the complete breakdown of all five budgeting methods below to choose the right one for you.

Step 4: Build Your Budget

Whichever method you choose, here’s the universal process for building a first budget that holds:

1. Start With Your Savings Goal

Before allocating a single expense, write down what you’re saving for and how much per month you need to get there. Put this number into your budget first. This isn’t idealistic—it’s structural. When savings appear first, they happen. When they appear last, they don’t.

If you’re not sure how much to save or where to put it, read our guide on how to build an emergency fund.

2. List Every Fixed Expense

Fixed expenses are the same or close to the same every month—rent, mortgage, car payment, insurance premiums, phone contract, internet, debt minimum payments. List them all. These don’t change month to month so they form your non-negotiable base.

3. Estimate Variable Expenses Honestly

Variable expenses change monthly—groceries, fuel, dining out, entertainment, clothing. Use your three-month average from your statement review in Step 2. Don’t estimate from memory. Memory is consistently optimistic.

4. Do the Math and Adjust

Income minus savings minus fixed expenses minus variable expenses should equal zero in a zero-based budget, or leave you within your allocated percentages in other frameworks.

If the numbers don’t work, you have two options: reduce expenses or increase income. Reducing fixed expenses requires negotiation or lifestyle changes. Reducing variable expenses is easier and produces faster results.

For specific tactics on cutting costs, see our guides on how to save money on a tight budget and how to save money on groceries.

The 5 Best Budgeting Methods Explained

Here are the five most proven personal budgeting methods, with honest guidance on who each one suits.

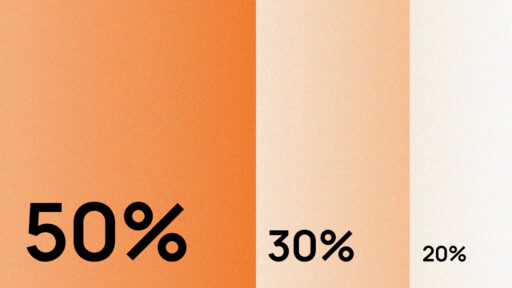

1. The 50/30/20 Rule

The simplest structured budgeting framework available. Divide your take-home pay into three categories:

- 50% — Needs (rent, utilities, groceries, transport, insurance, minimum debt payments)

- 30% — Wants (dining out, entertainment, travel, hobbies, subscriptions)

- 20% — Savings and extra debt repayment

Example Breakdown:

| Monthly Take-Home | 50% Needs | 30% Wants | 20% Savings |

|---|---|---|---|

| $2,500 | $1,250 | $750 | $500 |

| $3,500 | $1,750 | $1,050 | $700 |

| $5,000 | $2,500 | $1,500 | $1,000 |

| $7,000 | $3,500 | $2,100 | $1,400 |

What works: Three numbers instead of forty. No complex category tracking. Easy to apply immediately without setup. Works well for people who want structure without micromanagement.

What doesn’t work: If your housing costs exceed 50% of income—common in cities like New York, San Francisco, or London—the framework breaks without adjustment. In that case, compress the Wants bucket before touching the Savings percentage. The 20% savings target is the last number you reduce, never the first.

Who it suits: Budgeting beginners, people who find detailed tracking overwhelming, those with stable monthly income.

For a deeper analysis, read our complete guide: The 50/30/20 Rule: Does It Actually Work?

2. Zero-Based Budgeting

Every dollar of your income is assigned a purpose before the month begins. Income minus all assigned categories equals exactly zero—not because you spend everything, but because savings and investments are explicit line items in the budget.

Example Budget:

| Category | Assigned Amount |

|---|---|

| Rent | $1,200 |

| Groceries | $400 |

| Transport | $250 |

| Utilities | $150 |

| Emergency fund savings | $300 |

| Retirement contribution | $200 |

| Entertainment | $150 |

| Dining out | $200 |

| Everything else | $150 |

| Total (= your income) | $3,000 |

Zero-based budgeting is the most popular budgeting method overall, used by one-third of people (33.3%).

What works: Nothing falls through the cracks. Every savings goal is funded explicitly. Particularly powerful for people who want to eliminate debt or build savings aggressively.

What doesn’t work: Requires genuine monthly setup time—typically 30–60 minutes at the start of each period. If life changes significantly mid-month (irregular income, unexpected expense), the whole budget needs adjustment.

Who it suits: Detail-oriented people, those with specific savings goals, anyone serious about breaking the paycheck-to-paycheck cycle.

For the complete walkthrough, see: Zero-Based Budgeting: The Complete Beginner Guide

3. The Envelope System

Divide your monthly spending budget into physical or digital “envelopes”—one per spending category. When a category’s envelope is empty, spending in that category stops until the next month.

The method works because it creates a visceral, immediate connection between spending and its consequences. There’s no abstract mental accounting when you physically hand over the last $20 from your grocery envelope.

Digital versions of the envelope system are available through budgeting apps—Goodbudget is the most widely used digital envelope system currently available. Physical cash envelopes remain effective for people who find digital abstractions easy to ignore.

Who it suits: People who find it easy to rationalize overspending in the abstract but respond differently to concrete limits. People who have tried other methods and found them too easy to override mentally.

4. The Pay Yourself First Method

Rather than budgeting all categories and saving what remains, this method reverses the sequence: your savings transfer goes out the moment your paycheck arrives, before you allocate anything else.

The rest of the month’s spending is managed with whatever is left. This works because it removes savings from the equation of monthly spending decisions entirely.

Recent data shows that 72% of Gen Z took steps to improve their financial health over the last 12 months, with 51% putting money toward savings. The most consistent pattern among those who succeed at saving is automation—a transfer that happens without a decision being made each month.

Who it suits: People who know they should save but consistently find the month ending with nothing left. Anyone who benefits from removing willpower from financial decisions.

For more saving strategies, read: How to Save Money Fast: 21 Tricks That Actually Work

5. The Two-Account System

Keep two separate bank accounts. One receives your income and handles all fixed, non-negotiable expenses—rent, utilities, insurance, subscriptions, debt minimum payments, and a pre-set savings transfer. A second account receives a set weekly “spending money” transfer and covers all discretionary spending for the week.

When the spending account is empty, discretionary spending stops. Fixed obligations continue automatically from the primary account.

Who it suits: People who prefer not to track individual categories but need a structural limit on discretionary spending. Particularly effective for couples managing shared expenses alongside personal spending.

Budgeting Methods Comparison

| Method | Setup Time | Monthly Effort | Best For | Biggest Risk |

|---|---|---|---|---|

| 50/30/20 Rule | 30 minutes | Low—check weekly | Beginners, simple setup | Housing costs exceeding 50% |

| Zero-Based Budget | 60–90 minutes/month | Medium—update regularly | Specific savers, debt payoff | Mid-month income changes |

| Envelope System | 30 minutes | Low—envelopes do the work | Overspenders who need limits | Inflexibility when needs change |

| Pay Yourself First | 15 minutes | Very low—automated | Anyone, especially non-trackers | Under-budgeting variable expenses |

| Two-Account System | 20 minutes | Low—automatic structure | Couples, casual budgeters | Weekly spending account running dry |

Budget Categories and What They Should Cost

According to the Bureau of Labor Statistics Consumer Expenditure Survey, housing is the largest expense for American households, making up 32.9% of total spending in 2023. Nearly half of survey respondents—49%—said that rent or mortgage payments took up the biggest part of their budget.

Here’s a realistic target allocation for each major category, based on BLS data and financial planning benchmarks:

| Category | Recommended % of Take-Home | Average US Household Monthly |

|---|---|---|

| Housing (rent/mortgage) | 25–35% | ~$2,025 |

| Food (groceries + dining) | 10–15% | ~$830 |

| Transport | 10–15% | ~$650 |

| Utilities | 5–8% | ~$350 |

| Insurance | 4–6% | ~$280 |

| Savings and emergency fund | 10–20% | Target: 20% |

| Debt repayment (beyond minimums) | 5–15% | Depends on debt load |

| Entertainment and personal | 5–10% | ~$300 |

| Clothing | 2–4% | ~$150 |

| Healthcare out-of-pocket | 3–5% | ~$200 |

The Categories Most People Overspend

According to recent financial data, food delivery spending increased from $162.40 to $179 per month in 2025, up 10.2%, while gym membership spending jumped 19% from $85.50 to $101.80.

Subscription creep—gradual accumulation of recurring charges—continues to be one of the most consistent hidden budget drains across all income levels.

For complete guidance on tracking and cutting subscription spending, see our article on the best budgeting apps.

Budgeting by Life Stage: What Changes at Each Point

Personal budgeting isn’t a single static activity. The priorities shift significantly depending on where you are in life, what obligations you carry, and what goals are most relevant right now.

Budgeting in Your 20s

Building an emergency fund remains difficult for Gen Z—over half (55%) don’t have enough emergency savings to cover three months of expenses.

The 20s budget has two non-negotiable priorities above everything else: building an emergency fund and capturing any available employer retirement match. Both of these set up every other financial goal that follows.

The emergency fund creates the buffer that prevents a bad month from becoming debt. The employer match is free money being declined—often thousands of dollars annually—that compounds for decades.

Your 20s Budget Priorities:

| Priority | Target | Why It Can’t Wait |

|---|---|---|

| Emergency fund | 3 months expenses | Without this, every emergency becomes debt |

| Employer 401(k) match | Contribute enough to capture 100% | Average match: 4.4% of salary = free money |

| Student loan payments | Above minimum if possible | Interest compounds against you daily |

| Housing | Under 30% of take-home | Keeps flexibility for other priorities |

To get started with emergency savings, read our guide on how to build an emergency fund from zero.

Budgeting in Your 30s

The 30s typically bring the highest number of simultaneous financial pressures: mortgage or high rent, family costs, career advancement expenses, retirement savings that feel increasingly urgent, and often the beginning of genuine wealth-building.

Recent survey data shows that 49% of Millennials don’t have enough emergency savings to cover three months of expenses, a figure that has remained broadly consistent since 2022.

The 30s budget requires explicit priority ordering because there are more legitimate demands on income than most budgets can fully satisfy simultaneously.

Your 30s Budget Priorities:

| Priority | Target |

|---|---|

| Emergency fund | Fully funded at 3–6 months |

| Retirement contributions | 15% of gross income (including employer match) |

| Mortgage or housing | Under 28% of gross income |

| Children’s education fund | Start early—compound interest works here too |

| High-interest debt elimination | Aggressively above minimum payments |

Budgeting in Your 40s and 50s

The peak earning years—and the years where budgeting errors compound most expensively. Gen X reports the highest financial insecurity of any age group, with 54% saying they don’t feel financially secure.

The primary budget shift in your 40s is from accumulation to acceleration. Emergency fund is typically established. The focus moves to maximizing retirement contributions, eliminating remaining debt, and building taxable investment accounts alongside tax-advantaged ones.

The budget mistake most common in this decade: Lifestyle inflation that expands as income grows, preventing the savings acceleration that these income levels make possible.

Budgeting for Couples

The most common approach among couples is to combine their income and budget together (37.9%), while many others (23.5%) split bills but manage personal expenses separately. Over one in ten couples (10.8%) manage their budget completely separately.

There’s no universally correct approach. The approach that works is the one both partners genuinely agree on—and review together at least monthly.

Three models that consistently work:

- Full combination: All income pools together. All expenses paid from shared accounts. One budget covers everything. Works best when both partners have similar spending philosophies.

- Partial combination: Fixed shared expenses (rent, utilities, groceries) paid from a shared account funded proportionally. Personal spending managed separately. Works well when partners have significantly different incomes or spending styles.

- Complete separation: Each partner funds their own expenses. Shared costs split by agreement. Works best for couples who want financial independence within the relationship.

For detailed strategies, read: How to Budget as a Couple Without Fighting About Money

How to Make Your Budget Stick: The Practical Tactics

Building a budget is the easier part. Maintaining it across months when motivation fluctuates is where most people lose the thread.

Weekly Check-Ins: Ten Minutes, Not Thirty

The budgets that fail are reviewed never or monthly—by which point the damage is done and the review feels like an autopsy. The budgets that work are reviewed briefly and regularly.

Ten minutes once per week. Check your spending against your budget categories. Note which categories are running ahead. Adjust the remaining week accordingly. That’s it.

The frequency of contact with your budget is more important than the depth of any single review.

The Adjustment Rule: When Life Changes Mid-Month

Every budget will be broken by reality at some point. A car repair. A medical bill. A genuine opportunity that wasn’t in the plan.

The response that kills budgets: Treating the overspend as evidence that budgeting doesn’t work.

The response that maintains budgets: Treating it as a normal event that requires adjustment. Reduce the Wants allocation for the remainder of the month to absorb the unplanned expense. Note it as a reason to build a stronger emergency fund or a specific sinking fund for known irregular expenses.

Sinking Funds: The Technique That Prevents Budget Destruction

A sinking fund is a small, ongoing monthly savings allocation for a known but irregular future expense. Instead of your car insurance renewal destroying your budget in March, you save $X per month throughout the year so the money is already there.

Recommended Sinking Funds:

| Sinking Fund Category | Annual Cost Estimate | Monthly Saving Needed |

|---|---|---|

| Car maintenance and repairs | $1,200 | $100 |

| Annual insurance premiums | $600 | $50 |

| Medical deductibles and copays | $800 | $67 |

| Holiday gifts and travel | $1,000 | $83 |

| Home maintenance | $1,500 | $125 |

| Annual subscriptions | $400 | $33 |

Sinking funds transform one-time budget shocks into planned, manageable monthly expenses. They’re the single most underused budgeting technique available.

Best Budgeting Tools and Apps (2026)

According to usage research, 27% of young adults (18–29) prefer budgeting apps, while 39% of middle-aged adults (30–44) favor spreadsheets, and 43% of older adults (45–59) stick to pen and paper.

Every tool works. No tool works without the habit behind it. That said, here’s honest guidance on which tool suits which person.

Budgeting Tools Comparison

| Tool | Best For | Biggest Advantage | Biggest Limitation |

|---|---|---|---|

| Budgeting app (Monarch, YNAB) | Automatic trackers, busy people | Bank syncing, automated categorization | Monthly cost, setup time |

| Spreadsheet (Google Sheets, Excel) | Detail-oriented, customizers | Full control, free, highly flexible | Manual entry, easy to avoid opening |

| Pen and paper | Tactile learners, simplicity seekers | Deliberate awareness from manual recording | No automation, storage fragile |

| Two-account bank system | People who avoid tracking | Structural limit requires no tracking | Less insight into category spending |

Recommended Budgeting Apps (Editor’s Picks)

1. YNAB (You Need A Budget)

Best for: Zero-based budgeting enthusiasts and aggressive savers

Pros:

- Powerful zero-based budgeting methodology

- Excellent goal-tracking features

- Strong mobile app with bank sync

- Active user community and educational resources

Cons:

- Steeper learning curve than competitors

- Higher price point at $14.99/month or $99/year

- Requires commitment to the YNAB methodology

Pricing: $14.99/month or $99/year (34-day free trial)

2. Monarch Money

Best for: Users who want premium features with beautiful design

Pros:

- Clean, intuitive interface

- Automatic transaction categorization

- Net worth tracking and investment monitoring

- Collaborative budgeting for couples

- Custom budget categories

Cons:

- More expensive than some alternatives

- No free tier available

- Fewer third-party integrations

Pricing: $14.99/month or $99.99/year (7-day free trial)

3. EveryDollar

Best for: Ramsey Solutions followers and envelope budgeters

Pros:

- Simple, user-friendly interface

- Free version available

- Follows Dave Ramsey’s Baby Steps methodology

- Good for couples and families

Cons:

- Bank sync only available in premium version

- Limited reporting features

- Less flexible than some competitors

Pricing: Free basic version; Premium $79.99/year for bank sync

4. Rocket Money

Best for: Subscription management and bill negotiation

Pros:

- Identifies and cancels unwanted subscriptions

- Negotiates bills on your behalf

- Spending insights and budgets

- No monthly fee—only success fees for savings

Cons:

- Less robust budgeting features than dedicated apps

- Takes percentage of negotiated savings

- Limited customization options

Pricing: Free basic features; Premium $6-12/month based on income

Free Budget Templates

For those who prefer spreadsheets, we’ve compiled the best free templates available:

- Google Sheets Budget Template: Complete monthly budget with automatic calculations

- Excel Zero-Based Budget: Pre-formatted zero-based budgeting spreadsheet

- 50/30/20 Worksheet: Simple percentage-based budget calculator

Download all templates: Best Free Budget Spreadsheet Templates

The Connection Between Budgeting and Your Financial Goals

A personal budget isn’t an isolated financial activity. It’s the foundation beneath every other financial goal. Here’s how the pieces connect:

Budgeting and Saving Money

A budget without a savings line item is incomplete. The savings rate you target determines how quickly every other financial goal becomes reachable.

To understand what consistent saving actually looks like in practice, read our complete guide on how to save money fast.

Budgeting and Debt

Your monthly budget determines how quickly debt gets paid off. Extra debt payments—above minimum payments—are a budget category like any other. Understanding which debts to prioritize first changes how much you pay in total.

For the complete debt elimination framework, see: How to Pay Off Credit Card Debt Fast

Budgeting and Investing

Once your budget consistently produces a surplus above your emergency fund and debt payments, that surplus is investable. The path from budgeting to investment isn’t a leap—it’s the next logical allocation.

When you reach that point, start with our guide: How to Start Investing as a Beginner

Budgeting and Income

A budget that’s structurally impossible—where genuine essential expenses exceed take-home income regardless of cuts—has an income problem, not a spending problem. In that case, the other side of the equation needs attention.

For income-expanding strategies that complement a tighter budget, read:

Real Budget Success Stories

Tom, 28—Software Developer, Austin

Tom earned $82,000 per year and had $600 in savings. He had a vague sense of where his money went but no budget. He spent 90 minutes on a Sunday building his first zero-based budget.

What he found: $340 per month in subscriptions he’d forgotten about, $600 per month in food delivery he’d underestimated by almost half, and no line item for savings anywhere in his mental accounting.

He canceled unused subscriptions, reduced food delivery to Friday nights only, and automated a $500 savings transfer for every payday.

Twelve months later: $6,400 saved. First time since his student years he felt ahead rather than behind.

“The budget didn’t tell me what I couldn’t do. It told me why I had no money despite a good salary. Once I saw the actual numbers, the decisions made themselves.”

Danielle and Marcus, 34 and 36—Teachers, Philadelphia

Research shows that married people are more likely to be happy with their finances compared to singles—61% versus 37%. Danielle and Marcus weren’t in that 61%. They were in different financial philosophies in the same household, which produced monthly arguments about money and no shared plan.

They built a partial combination budget—shared account for housing, utilities, and groceries; individual accounts for personal spending. Each funded the shared account proportionally based on their salaries. Personal spending required no justification to the other.

Six months later: No money arguments. First family holiday paid in cash in four years.

When asked what one word described their financial outlook for 2026, 32% of US adults chose “hopeful” and 26% chose “confident.” Both Danielle and Marcus now use both words.

The Three Budget Mistakes That Derail Almost Everyone

Mistake 1: Budgeting from Last Month’s Ideal, Not This Month’s Reality

If last month had an unusual expense—a medical bill, a car repair, a one-off celebration—don’t pretend next month starts from zero. Factor in what you know is coming.

Mistake 2: No Buffer Category

Every realistic budget includes a small miscellaneous allocation—$50–$150 per month—for genuinely unexpected small expenses. Without it, every small surprise breaks the plan and the plan feels unreliable.

Mistake 3: Setting the Savings Target Too High, Too Soon

Financial data shows that medium-income earners are most likely to stay on budget—66%—while those at the extremes of the income spectrum struggle most.

Ambitious savings targets that genuinely can’t be maintained within a real budget get reduced quietly and eventually abandoned.

A $200 monthly savings target that’s actually maintained for twelve months produces $2,400.

A $600 target maintained for two months then abandoned produces $1,200.

Sustainable beats ambitious.

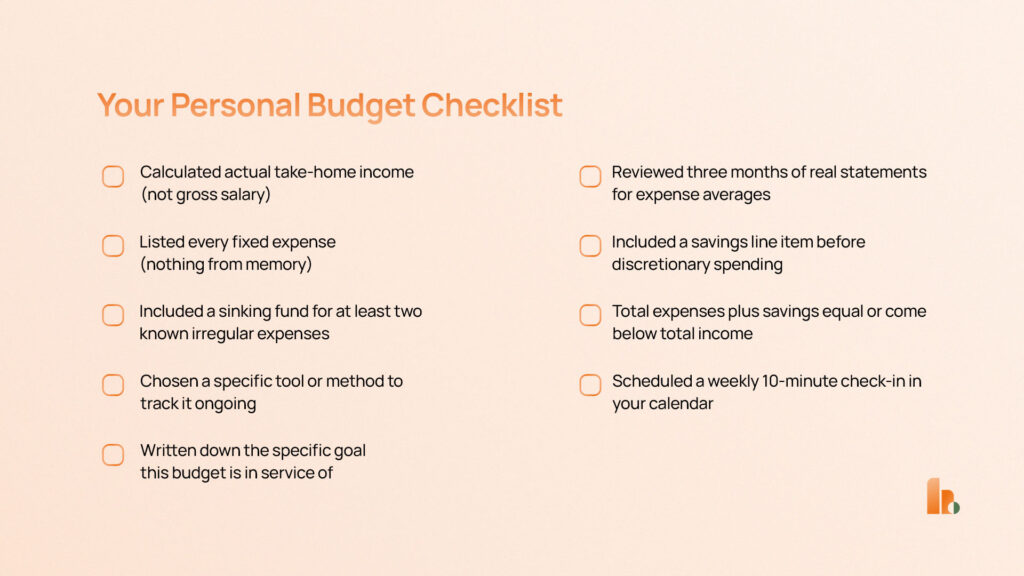

Your Personal Budget Checklist

Before your budget goes into effect, run through this:

- ✅ Calculated actual take-home income (not gross salary)

- ✅ Reviewed three months of real statements for expense averages

- ✅ Listed every fixed expense (nothing from memory)

- ✅ Included a savings line item before discretionary spending

- ✅ Included a sinking fund for at least two known irregular expenses

- ✅ Total expenses plus savings equal or come below total income

- ✅ Chosen a specific tool or method to track it ongoing

- ✅ Scheduled a weekly 10-minute check-in in your calendar

- ✅ Written down the specific goal this budget is in service of

A budget that passes all nine checks is a budget that can work. Not a guarantee—but a foundation.

Frequently Asked Questions

What is personal budgeting and why does it matter?

Personal budgeting is a forward-looking plan that directs your income to specific purposes—expenses, savings, and debt repayment—before it’s spent. It matters because over 84% of people who budget consistently report that it has helped them either avoid debt or pay it off, and because financial goals—saving for a home, building an emergency fund, retiring comfortably—are structurally impossible without a plan that funds them deliberately.

What is the best budgeting method for beginners?

The 50/30/20 rule is the most accessible starting point for most beginners—it requires no complex category tracking, applies immediately to any income level, and is flexible enough to adjust as your financial situation changes. Zero-based budgeting produces stronger results for people with specific savings goals or debt they want to eliminate aggressively, but requires more setup time. Start with the simplest method you’ll actually maintain, then add complexity as the habit establishes itself.

How much of my income should go toward savings in my budget?

The standard recommendation is 20% of take-home pay, as outlined in the 50/30/20 framework. Recent survey data shows that two-thirds of respondents (66%) include savings as part of their budget, while one-third do not budget money for savings at all. If 20% isn’t immediately achievable, start with whatever percentage you can maintain consistently and increase by 1–2% every three to six months.

How do I stick to my budget when unexpected expenses come up?

Build a miscellaneous buffer of $50–$150 per month into your budget for small unexpected costs. For larger irregular expenses—car repairs, medical bills, annual insurance premiums—build sinking funds: small monthly allocations that accumulate throughout the year so the money is already available when the expense arrives. Treat unexpected expenses that exceed both buffers as a reason to reduce discretionary spending that month, not as evidence that budgeting is impossible.

What is the difference between a budget and just tracking expenses?

Expense tracking tells you where money went after it left. A budget tells money where to go before it leaves. Tracking is retrospective—useful for understanding patterns but unable to change the outcomes that have already occurred. A budget is prospective—it changes the decisions you make in real time. Most effective personal finance systems combine both: a monthly budget built in advance and weekly tracking to monitor progress against it.

How often should I review and update my personal budget?

Review your budget against actual spending once per week—a ten-minute check is sufficient. Do a full monthly budget build at the start of each new month, adjusting for any category that changed significantly. Review your overall budget structure every six months or whenever a major life change occurs—a salary increase, a new debt, a significant expense category that appears or disappears, or a financial goal that has been achieved and needs replacing with a new one.

Can I use budgeting apps if I have irregular income?

Yes. If you’re freelance, commission-based, or have seasonal income, use zero-based budgeting with a conservative baseline. Calculate your average monthly income using your three lowest-earning months from the past year, then budget from that floor. Any income above that baseline can be allocated to savings, extra debt payments, or building a larger buffer. Apps like YNAB and Monarch handle irregular income well with their flexible allocation features.

Should couples combine finances or keep them separate?

There’s no universally correct approach. The most common method is full combination (37.9% of couples), followed by splitting bills while keeping personal expenses separate (23.5%), and complete separation (10.8%). The approach that works is the one both partners genuinely agree on and review together at least monthly. For detailed strategies on each model, read our guide on budgeting as a couple.

Sources

All statistics and data in this guide are sourced from the following verified sources:

- SoFi Personal Finance Survey 2025

- Debt.com Budgeting Survey 2025

- Ramsey Solutions State of Personal Finance Q4 2025

- YouGov Financial Health Survey 2025

- WalletHub Budgeting Statistics 2025

- Empower Wealth Watch 2025

- Self Financial Household Budget Survey 2025

- Bank of America Better Money Habits 2025

- Moneywise Personal Finance Statistics 2025

- Bureau of Labor Statistics Consumer Expenditure Survey 2023

- National Endowment for Financial Education Polls 2025–2026

- NerdWallet Financial Health Survey 2025

- Yahoo Finance New Year’s Resolutions Study 2026

- USAFacts Financial Security Report 2025

- The Motley Fool Consumer Finance Survey 2024

- Carry Budget Tracking Research 2025

Ready to start your budgeting journey? Download our free budget templates or explore our recommended budgeting apps to begin building your financial foundation today.

{kind=link}